Foreclosure headlines are getting attention again, and it is easy to understand why. When homeowners hear that foreclosure activity is rising, many immediately think back to 2008 and wonder if the housing market is heading toward another crash.

That concern is understandable, but the full picture matters. Today’s foreclosure activity is increasing from unusually low levels, and the current housing market has several major differences from the last downturn. For homeowners in the greater Tampa Bay area, especially across Hillsborough and Pinellas counties, the key is understanding what the numbers really mean and what options may be available if financial pressure is starting to build.

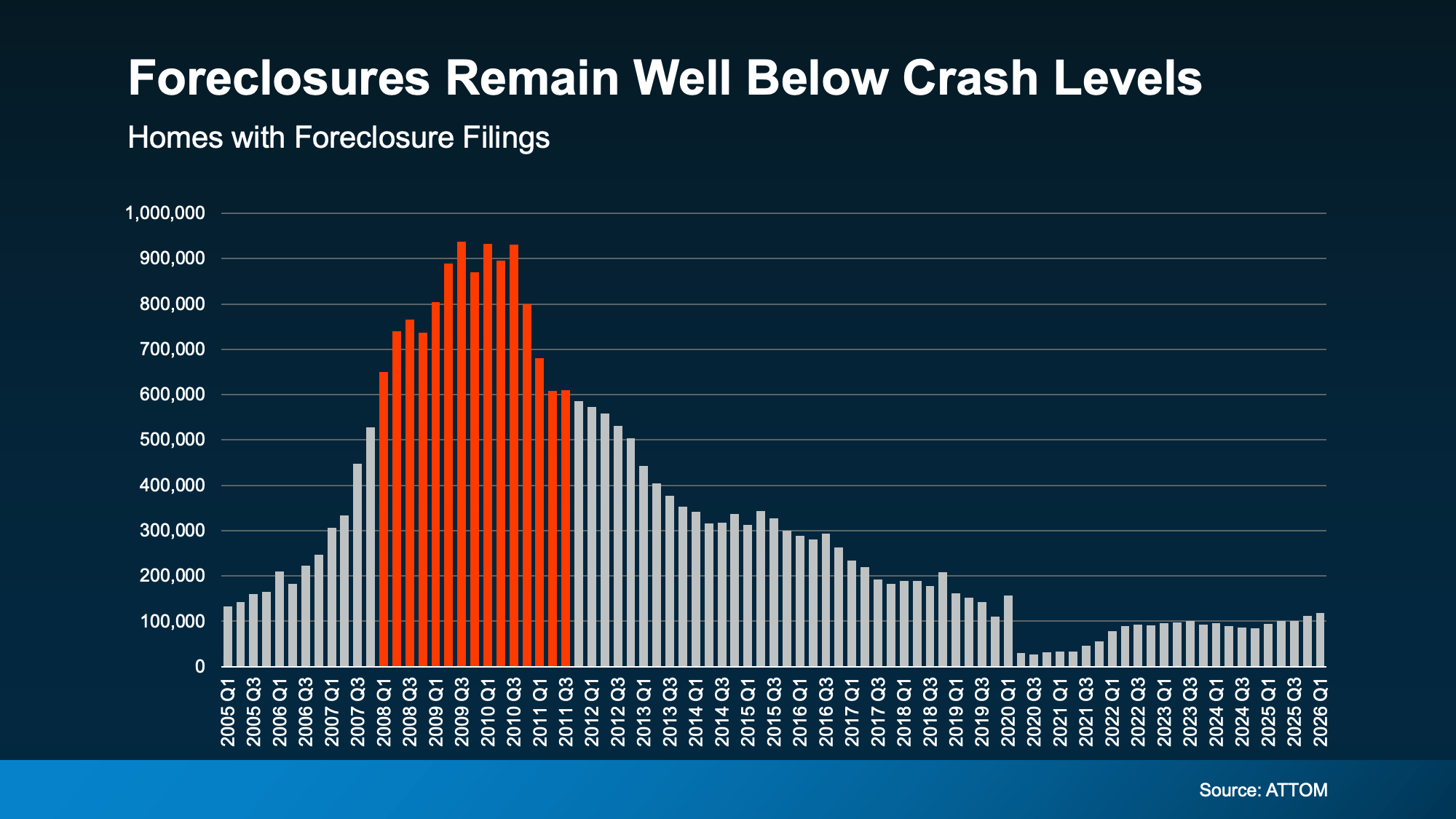

Foreclosure filings are up 26% compared to a year ago, and they have been rising for 5 straight quarters. That is a real trend, and it should not be ignored. But rising activity does not automatically mean the market is crashing.

A big reason the numbers look more dramatic is because foreclosure activity was extremely low in 2020 and 2021. During that period, pandemic related protections and moratoriums kept many foreclosure proceedings from moving forward. Those years were not normal market conditions, so they are not the best baseline for comparison.

A more useful comparison is the pre-pandemic market in 2017, 2018, and 2019. When today’s foreclosure numbers are viewed against those more normal years, activity is still lower than it was before the pandemic. That points more to a market moving back toward normal than a market falling apart.

This distinction matters for Tampa Bay homeowners because headlines can create unnecessary panic. While some owners are facing real financial strain from higher insurance costs, taxes, interest rates, and everyday expenses, the broader foreclosure picture still looks very different from 2008.

One of the biggest differences between now and the last housing crash is homeowner equity. In 2008, many homeowners owed more on their mortgages than their homes were worth. That left them with very few options if they fell behind.

Today, many homeowners have built substantial equity because of the price growth that happened over the past several years. Even if values have softened in some neighborhoods, a large number of owners still have room between what they owe and what their home could sell for.

That equity can create options. A homeowner who is behind on payments may be able to sell, pay off the mortgage, cover selling costs, and avoid a completed foreclosure. In some cases, they may still walk away with proceeds that can help them reset financially.

This is especially important in areas like Riverview, Brandon, Tampa, St. Petersburg, Clearwater, and surrounding communities where values rose sharply after 2020. Every situation is different, but equity can be the difference between feeling trapped and having a path forward.

Another important detail is that a foreclosure filing does not always mean the homeowner loses the home. A filing means the process has started, but many cases are resolved before they reach the final stage.

Some homeowners work out repayment plans with their lender. Others may qualify for forbearance, a loan modification, or another loss mitigation option. Some decide that selling is the most practical move before the situation gets worse.

The gap between foreclosure filings, foreclosure starts, and completed foreclosures tells a more balanced story. Filings can rise while completed foreclosures remain much lower because many homeowners find another solution before the process reaches the end.

For Florida homeowners, timing is especially important. Florida is a judicial foreclosure state, which means the lender generally has to go through the court system before a foreclosure sale can happen. That process gives homeowners a chance to respond, explore options, and make informed decisions, but it does not mean they should wait until the last minute.

The 2008 housing crash was fueled by a very different set of conditions. Risky lending, weak underwriting, falling home values, and widespread negative equity created a situation where many homeowners had no practical way out.

Today’s market has challenges, but they are different challenges. Affordability is tight. Insurance costs are higher. Some homeowners are stretched. Buyers are more cautious, and homes are not selling as quickly as they did during the peak pandemic market.

But most homeowners are not in the same equity position they were in during the last crash. Lending standards have also been much stronger for years, which means the foundation of the current market is different.

That does not mean every homeowner is safe from financial trouble. It means the overall foreclosure increase should be viewed with context. Rising foreclosure activity is worth watching, but it is not the same as a repeat of the last housing crash.

If you are behind on payments or worried that you may fall behind, the most important step is to act early. Waiting usually reduces your options. Reaching out to your lender sooner can give you more room to explore repayment plans, temporary forbearance, loan modification, or other solutions.

It is also smart to understand your home’s current market value. In a shifting market, online estimates may not be accurate enough to make a major financial decision. A real valuation should look at recent comparable sales, active competition, condition, location, buyer demand, and what similar homes are doing right now.

For sellers in Hillsborough or Pinellas County, this matters because pricing strategy can make a major difference. If selling is the right option, the goal is not just to list the home. The goal is to price it correctly, market it well, and move before the pressure becomes harder to manage.

Foreclosure activity is rising, but today’s numbers are still nowhere near 2008 levels. The market is moving away from the unusually low foreclosure activity of the pandemic years, not necessarily toward another housing crash.

Home equity is the biggest reason this cycle looks different. Many homeowners have options today that were not available to people who were underwater during the last crash.

If you are a Tampa Bay homeowner facing financial pressure, do not assume foreclosure is inevitable. The sooner you understand your numbers, talk to your lender, and evaluate your home’s value, the more control you may have over the outcome.