Many Veterans and active duty service members feel like buying a home is out of reach right now. That is understandable. Home prices, mortgage rates, insurance costs, taxes, and everyday expenses have made affordability a real challenge for many buyers.

But some Veterans may be closer to homeownership than they realize. The VA home loan benefit can remove or reduce some of the biggest barriers that keep buyers on the sidelines.

For eligible Veterans, service members, and qualifying surviving spouses in the greater Tampa Bay area, the key is understanding what the VA loan benefit actually offers. A lot of buyers have heard of VA loans, but many do not fully understand how powerful the benefit can be.

A VA loan is not just another mortgage option. It is a benefit designed to help eligible Veterans, service members, and surviving spouses buy a home with terms that may be more favorable than many conventional loan options.

The biggest advantage is that VA loans can allow eligible buyers to purchase with $0 down. That does not mean there are never costs involved, and it does not mean every buyer automatically qualifies for every home. But it can remove one of the biggest hurdles buyers face, which is saving for a large down payment.

For Tampa Bay buyers, that can make a meaningful difference. In areas like Tampa, Riverview, Brandon, St. Petersburg, Clearwater, and surrounding communities, saving 3%, 5%, or 10% down can take a long time. If a qualified buyer can use a VA loan with $0 down, the timeline to purchase may be much shorter than they expected.

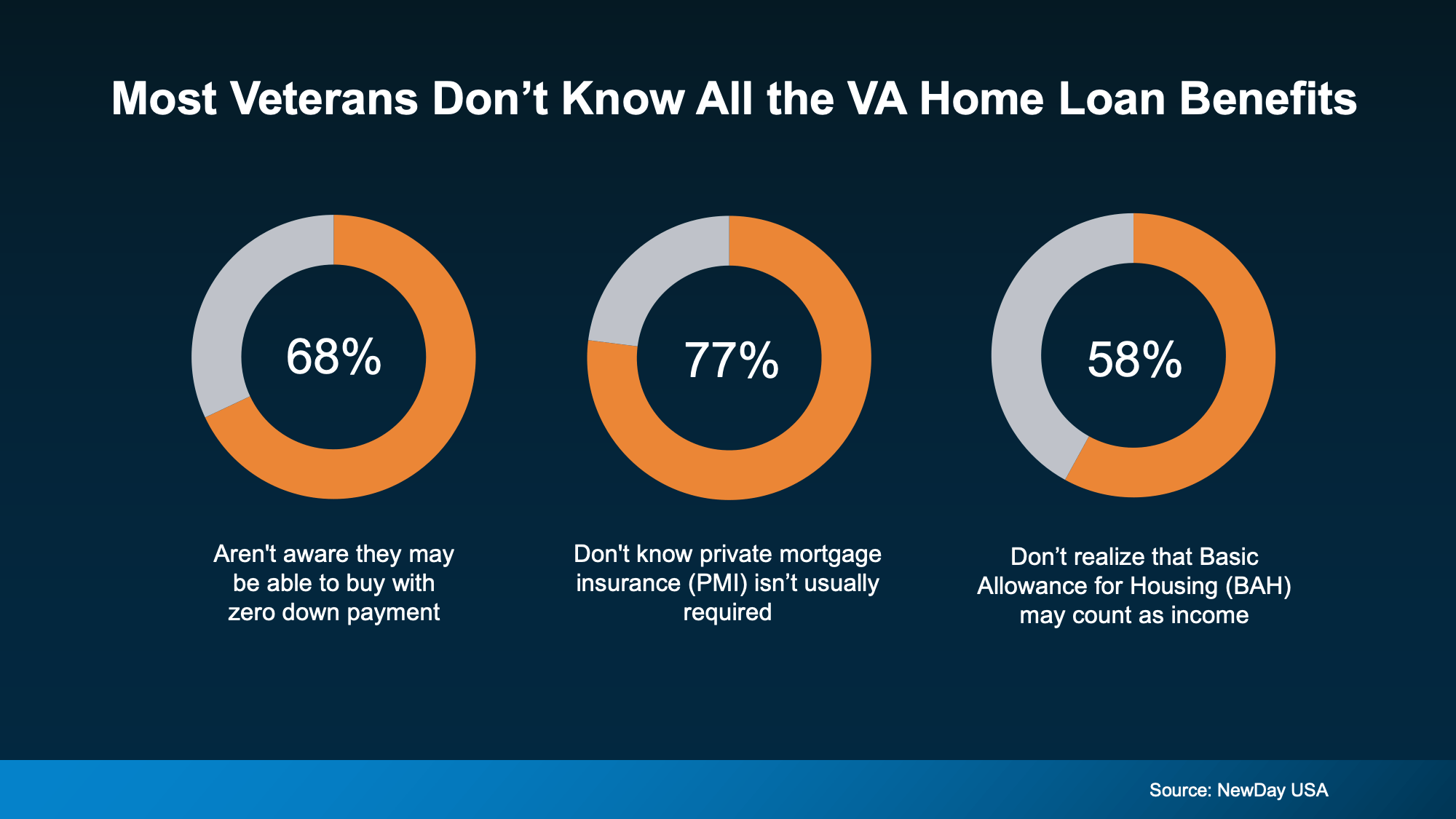

One of the most misunderstood VA loan benefits is the potential to buy without a down payment. Many Veterans assume they need to save tens of thousands of dollars before they can even start looking seriously.

That is not always true. For many eligible VA buyers, $0 down may be possible, depending on lender approval, income, credit, entitlement, property eligibility, and contract terms.

This can be especially helpful for first-time buyers who have stable income but have not built up a large savings account yet. Instead of waiting years to save a down payment, a VA buyer may be able to focus more on cash reserves, closing costs, inspections, moving expenses, and long-term affordability.

That said, $0 down should still be used wisely. Buyers should make sure the monthly payment fits comfortably, especially in Florida where homeowners insurance, property taxes, flood insurance, HOA fees, and CDD fees can change the affordability picture.

Another major benefit is that VA loans do not require monthly private mortgage insurance. With many conventional loans, buyers who put less than 20% down may have to pay PMI as part of the monthly payment.

That extra monthly cost can add up quickly. Avoiding PMI can help a VA buyer qualify more comfortably or keep the payment lower compared to another loan option with similar purchase terms.

This is one reason VA financing can be so valuable in today’s market. When buyers are already dealing with higher rates and higher monthly costs, removing monthly mortgage insurance can help improve affordability.

VA loans may still include a VA funding fee unless the buyer is exempt. That fee is different from monthly PMI. Depending on the buyer’s eligibility, military category, down payment, and whether the benefit has been used before, the funding fee may vary and may often be financed into the loan.

VA loans can also limit certain buyer closing costs. That does not mean a VA buyer has no closing costs. Buyers may still have lender charges, prepaid taxes and insurance, escrow setup costs, inspections, appraisal costs, title related costs, and other expenses depending on the transaction.

But VA rules can restrict what the Veteran is allowed to pay in certain categories. That can help reduce the amount of cash needed at closing compared to what some buyers assume.

In addition, seller concessions may be negotiated in the contract. In a market where some sellers are more flexible, a VA buyer may be able to ask for help with closing costs, prepaid expenses, or other allowable concessions.

The important point is this. A Veteran should not assume the cash needed to buy is the same as a conventional loan. The only way to know is to have a lender run the numbers using the buyer’s actual income, credit, entitlement, debt, and target purchase price.

For active duty service members and some qualifying reservists, Basic Allowance for Housing and Basic Allowance for Subsistence may count toward qualifying income. That can make a meaningful difference when a lender is calculating buying power.

BAH and BAS are also generally non-taxable, which may help them carry more weight in the qualification process compared to taxable income. If a service member is trying to estimate what they can afford without including those allowances, they may be underestimating their true qualifying income.

This is especially relevant around areas with military presence and commuting access to MacDill Air Force Base. Service members comparing Tampa, Brandon, Riverview, Apollo Beach, St. Petersburg, or other nearby areas should make sure their lender understands VA financing and military income structure.

Not every lender handles VA files with the same level of experience. A buyer using BAH, BAS, VA disability income, PCS timelines, or other military-specific income details should work with a lender who understands how to document and structure the loan correctly.

A VA loan can be powerful, but it is not a shortcut around good financial planning. Buyers still need to look carefully at the full monthly payment and the long-term fit of the home.

In Florida, the payment is not just principal and interest. Buyers need to account for homeowners insurance, possible flood insurance, property taxes, HOA fees, CDD fees, maintenance, utilities, and future repairs. A $0 down option can help with cash upfront, but the monthly payment still needs to be sustainable.

Buyers should also remember that VA loans have property standards. The home must meet certain requirements, and issues discovered during appraisal or inspection can affect the transaction. That does not mean the home has to be perfect, but it does mean buyers should understand how VA property requirements may apply.

This is where preparation matters. A strong VA buyer should have a clear pre-approval, understand their cash needed to close, know what payment range is comfortable, and work with professionals who understand how to present and negotiate VA offers effectively.

VA home loans can make homeownership more accessible for eligible Veterans, active duty service members, and qualifying surviving spouses. The ability to buy with $0 down, avoid monthly PMI, and potentially reduce certain closing cost hurdles can make a major difference.

But the benefit is often misunderstood. Some buyers assume they need far more cash than they actually do, while others do not realize how BAH, BAS, or other military income may affect their qualification.

For Tampa Bay Veterans and service members, the smartest next step is to get clear numbers from a lender who understands VA loans. Once you know your eligibility, payment range, cash needed, and buying power, you may find that homeownership is closer than it seemed.