The real estate market is becoming more negotiable. Buyers are increasingly requesting help with closing costs, repairs, mortgage rates, and other expenses, while more sellers and home builders are considering those requests to complete a sale.

That does not mean every Tampa Bay buyer will receive a major discount or that every seller must agree to unfavorable terms. It means both sides should understand how concessions and incentives work, what may be negotiable, and how each request affects the complete financial terms of the transaction.

A seller concession is something the homeowner agrees to provide while negotiating an offer or resolving an issue during the transaction. Common examples include contributing toward the buyer’s closing costs, providing a repair credit, paying for an agreed service, or helping reduce the buyer’s mortgage costs.

A builder incentive is usually promoted before the buyer submits an offer. Builders may advertise closing cost assistance, mortgage rate buydowns, design upgrades, appliance packages, or reduced prices to attract buyers to a particular community or completed inventory home.

The terms are sometimes used interchangeably, but the distinction matters. A concession is commonly negotiated as part of the individual transaction, while an incentive is generally offered upfront under specific builder requirements.

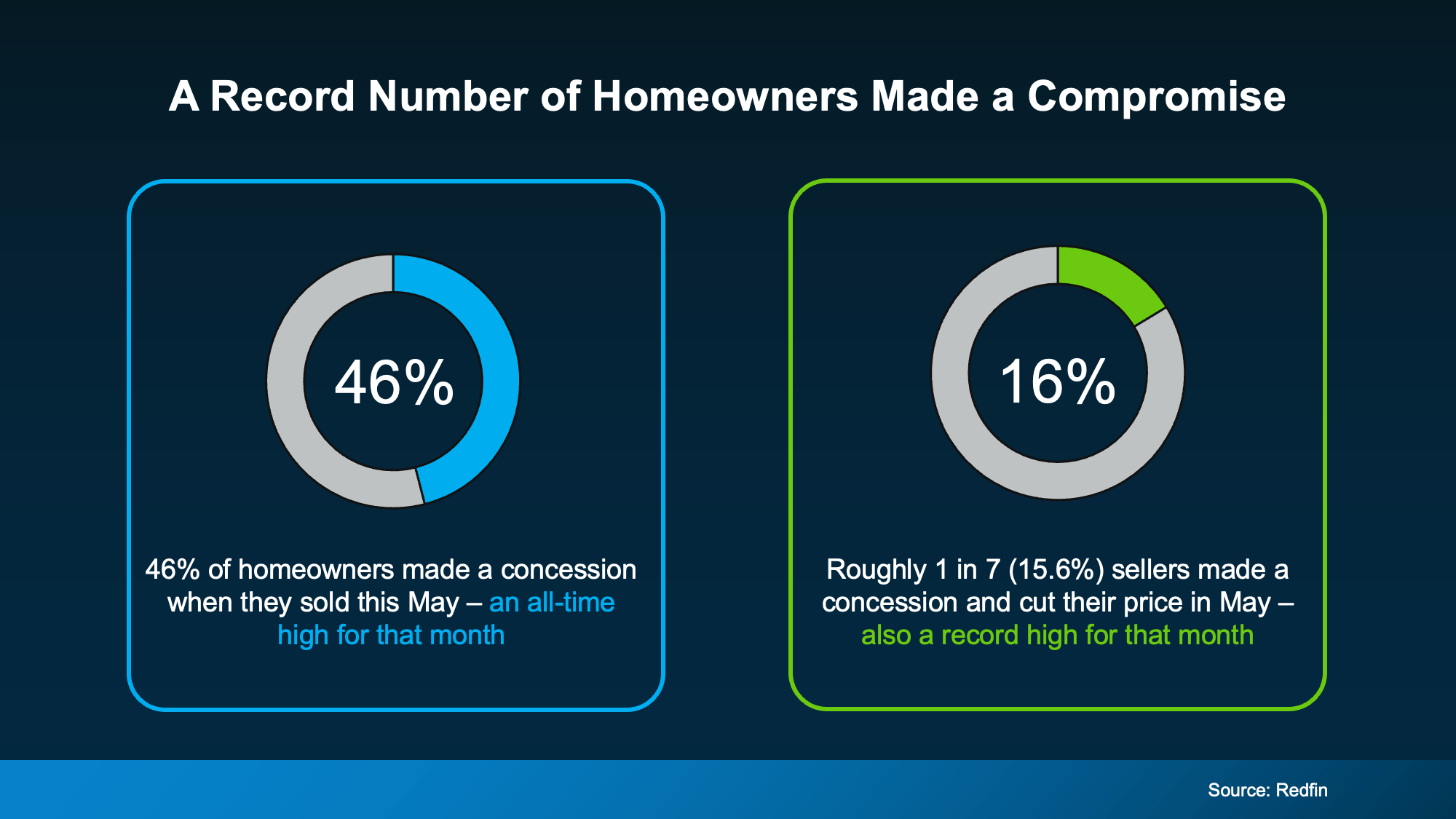

The source material reports that 46% of recent home sellers provided some form of concession to the buyer. Approximately 16% reduced their asking price and provided an additional concession within the same transaction.

These figures indicate that buyers may have more room to negotiate than they did during the highly competitive seller’s markets of previous years. Increased housing inventory, affordability challenges, longer market times, and competition from new construction can all motivate a seller to consider reasonable terms.

A seller may prefer to provide a credit rather than complete a repair before closing. Another seller may agree to help with closing costs while remaining firm on the purchase price because the higher recorded sale price is important to the transaction.

The right request depends on the property, competing offers, inspection results, financing, appraisal, and the seller’s priorities. Buyers should avoid assuming that every listing will include the same level of flexibility.

Closing cost assistance is one of the most common requests because it can reduce the amount of cash a buyer needs at closing. Depending on the loan and transaction, a seller contribution may help cover eligible lender charges, title expenses, prepaid taxes, homeowners insurance, mortgage insurance, or other approved costs.

Buyers may also request a credit toward repairs identified during the inspection. This can be preferable to asking the seller to hire a contractor because the buyer may want control over the company, materials, and timing after becoming the owner.

A mortgage rate buydown may be another option. Rather than requesting the same amount as a price reduction, a buyer can ask whether using the funds toward eligible financing costs would provide a greater monthly payment benefit.

The lender and closing professionals must confirm how a concession can be used. Buyers should review the proposed terms before submitting an offer so the requested amount is practical, properly written, and consistent with their loan.

Buyers should compare the full transaction rather than focusing only on the amount of the concession. A seller offering $10,000 toward closing costs may have priced the property higher than a comparable home offering no credit.

Property condition also matters. A substantial concession may not offset the cost of an aging roof, outdated electrical system, plumbing concerns, flood exposure, rising association expenses, or deferred maintenance.

The strongest offer strategy considers the purchase price, estimated value, monthly payment, cash required at closing, repairs, insurance, property taxes, HOA fees, CDD assessments, and expected ownership costs. A large advertised credit does not automatically make a property affordable or appropriately priced.

Sellers should expect more buyers to ask for concessions, but every request should be evaluated according to its effect on the seller’s estimated proceeds and likelihood of closing. A slightly higher offer that includes closing cost assistance may produce a similar result to a lower offer without a credit.

The strength of the buyer’s financing is also important. Sellers should consider the loan type, preapproval, escrow deposit, inspection terms, appraisal provisions, requested closing date, and other contingencies instead of evaluating the price alone.

A concession may be worthwhile when it resolves a legitimate concern, keeps a qualified buyer in the transaction, or produces an acceptable net result. Refusing every request could cause a property to remain on the market longer, particularly when buyers have several comparable homes available.

Sellers should not agree to unnecessary concessions simply because buyers are asking. Accurate pricing, strong presentation, proper marketing, and a clear understanding of current competition can protect the seller’s position during negotiations.

Home builders are also responding to affordability concerns and increased competition. The source material reports that 62% of builders were offering incentives, while 35% were reducing prices.

Builder incentives may include mortgage rate buydowns, closing cost contributions, reduced lot premiums, appliance packages, upgraded finishes, or adjustments to the purchase price. Completed inventory homes may have stronger incentives because the builder wants to sell the property and reduce ongoing carrying costs.

Some offers require the buyer to use the builder’s preferred lender or title company. Buyers should compare the complete loan estimate, interest rate, lender charges, purchase price, incentives, and long-term payment before deciding that the advertised package is the best financial option.

A buyer should also review HOA fees, CDD assessments, estimated property taxes, insurance costs, warranty coverage, completion timelines, and included features. Model homes often display upgrades that are not included in the advertised base price.

The builder’s sales representative works for the builder. Their role is to sell the property and protect the builder’s interests, even when they provide useful information and professional service.

A real estate professional representing the buyer can help compare communities, evaluate resale competition, review builder incentives, identify additional costs, and negotiate available terms. Representation should begin before the buyer registers or signs documents with the builder because builder policies may affect whether the buyer’s agent can participate.

New construction contracts are generally written by the builder and can differ significantly from standard resale contracts. Buyers should understand deposit requirements, financing deadlines, construction changes, completion dates, inspections, warranties, cancellation provisions, and what happens if the home does not appraise at the contract price.

Negotiating leverage varies throughout the Tampa Bay market. A buyer considering a home in Riverview, Brandon, FishHawk, South Tampa, Westchase, or Seminole Heights may encounter different inventory and competition than someone searching in St. Petersburg, Clearwater, Largo, Seminole, or Palm Harbor.

Property type also changes the conversation. A single-family home, townhome, condominium, and newly built property may each have different insurance requirements, association expenses, financing restrictions, maintenance concerns, and buyer demand.

A listing that is new to the market and receiving several showings may offer limited flexibility. A property that has been available for an extended period, returned to the market, or undergone several price reductions may provide greater negotiating room.

Local market data should be combined with property-specific information. The most useful comparison is not what sellers are offering nationally, but what similar Tampa Bay properties are accepting within the same area and price range.

Requesting a concession does not require submitting a weak offer. Buyers can improve the overall proposal with a meaningful escrow deposit, reliable financing, realistic inspection terms, complete documentation, and a closing date that works for the seller.

The request should also have a clear purpose. Asking for a specific amount toward eligible closing costs or an identified repair is usually stronger than submitting a broad demand without supporting numbers.

Buyers should remain focused on the total outcome. Winning every individual negotiating point is less important than purchasing the right property under terms that fit the buyer’s budget and protect their interests.

Sellers can reduce potential concession requests by addressing visible maintenance concerns before listing. Providing information about the roof, HVAC system, electrical panel, plumbing, insurance history, permits, flood zone, wind mitigation features, and recent improvements may also help buyers evaluate the property with greater confidence.

Pricing should reflect current conditions rather than past market expectations. Starting too high and later offering a large concession may be less effective than entering the market at a competitive price that generates stronger initial interest.

Sellers should calculate estimated proceeds under several possible scenarios before receiving offers. Understanding the effect of a price reduction, closing cost credit, repair allowance, or mortgage rate buydown makes it easier to respond strategically instead of reacting under pressure.

Seller concessions and builder incentives are becoming more common as buyers gain additional choices. The source data shows that 46% of recent sellers provided a concession, while 62% of builders offered incentives and 35% reduced new construction prices.

Buyers should consider asking for reasonable assistance, but every advertised credit must be evaluated as part of the complete purchase price, financing, property condition, and monthly cost. Sellers should remain open to terms that help complete a strong transaction while protecting their net proceeds and larger goals.

We can help buyers and sellers evaluate realistic concessions, compare new construction incentives, and negotiate based on current conditions throughout Hillsborough County, Pinellas County, and the greater Tampa Bay area.