The 1st half of 2026 required patience from both home buyers and sellers. Mortgage rates remained higher than many people hoped, affordability stayed challenging, and some households delayed their plans while waiting for clearer direction.

The 2nd half of the year may not produce a dramatic market reset, but several forecasts point toward the possibility of gradual improvement. Mortgage rates could ease, home prices are expected to remain relatively stable, and more buyers and sellers may decide they are ready to move.

For anyone considering a move in the Tampa Bay area, national forecasts are only a starting point. Housing conditions can vary significantly between Hillsborough County and Pinellas County, as well as between individual cities, neighborhoods, price ranges, and property types.

Mortgage rates are influenced by inflation, economic expectations, bond markets, and investor activity. When inflation remains elevated, mortgage rates are generally less likely to make a substantial decline.

The source data compares average oil prices with 30 year fixed mortgage rates and shows that both have often responded to similar economic pressures. Lower energy costs could help inflation improve, but they do not guarantee that mortgage rates will immediately decline.

The exact timing and size of any rate change cannot be predicted with certainty. Buyers should be cautious about postponing a purchase solely because they expect a significantly lower mortgage rate later in the year.

If rates decline, more buyers may return to the market at the same time. That increased competition could reduce negotiating opportunities and create upward pressure on prices for desirable, properly priced homes.

A more practical approach is to speak with a qualified lender and compare several payment scenarios. Buyers can review how different interest rates, purchase prices, down payments, seller credits, and temporary rate buydowns would affect their monthly expenses.

The mortgage rate is only 1 part of a Tampa Bay home buyer’s monthly payment. Property taxes, homeowners insurance, flood insurance, mortgage insurance, HOA fees, and CDD assessments can all affect affordability.

Insurance and flood considerations are especially important when comparing homes across Hillsborough and Pinellas counties. A property with a lower purchase price may not be the more affordable choice if its insurance, association fees, or expected maintenance costs are substantially higher.

Buyers should request realistic estimates before making an offer. A lender can calculate the projected mortgage payment, while an experienced local real estate professional can help identify property specific costs that may not be obvious from the listing price.

Many prospective buyers are waiting for home prices to fall. Although some cities and property types may experience declines, the national forecasts in the source material do not predict a broad price collapse during 2026.

The forecasts range from 0.6% to 4.0% growth, with an average projected increase of 2.3% for the year. FHFA data referenced in the source showed national prices approximately 1.7% higher than 1 year earlier, suggesting that price growth would need to strengthen modestly during the 2nd half to reach the average forecast.

This does not mean every Tampa Bay property will increase by 2.3%. National averages combine thousands of markets and cannot account for the differences between a South Tampa home, a Riverview subdivision, a St. Petersburg bungalow, or a Clearwater condominium.

Property condition, location, insurance costs, flood exposure, available inventory, association finances, and buyer demand can all influence value. Even homes within the same neighborhood may receive different results based on updates, presentation, pricing, and lot characteristics.

Buyers should not assume that delaying a purchase will automatically result in a lower home price. A future decline in mortgage rates could increase demand, bringing more competition into the market before inventory has enough time to adjust.

A lower rate may improve purchasing power, but that benefit could be partly offset if prices rise or sellers become less willing to negotiate. Buyers should evaluate the complete financial picture instead of trying to perfectly time 1 market factor.

The right time to buy depends on income stability, available savings, anticipated length of ownership, monthly budget, and personal plans. A forecast may help guide the conversation, but it should not replace a detailed review of the buyer’s actual finances.

Modest national price growth can be encouraging for sellers, but it does not mean every home can be listed above its market value. Buyers have access to more information and will compare a property with nearby listings, recent sales, available new construction, and alternative neighborhoods.

Homes that are priced appropriately and presented well may attract stronger interest. Properties that begin too high can accumulate market time, require price reductions, and create the impression that something is wrong with the home.

Tampa Bay sellers should base their strategy on recent comparable sales, active competition, current buyer activity, and the property’s condition. A price that reflects the local market is more useful than a national forecast or an automated online estimate.

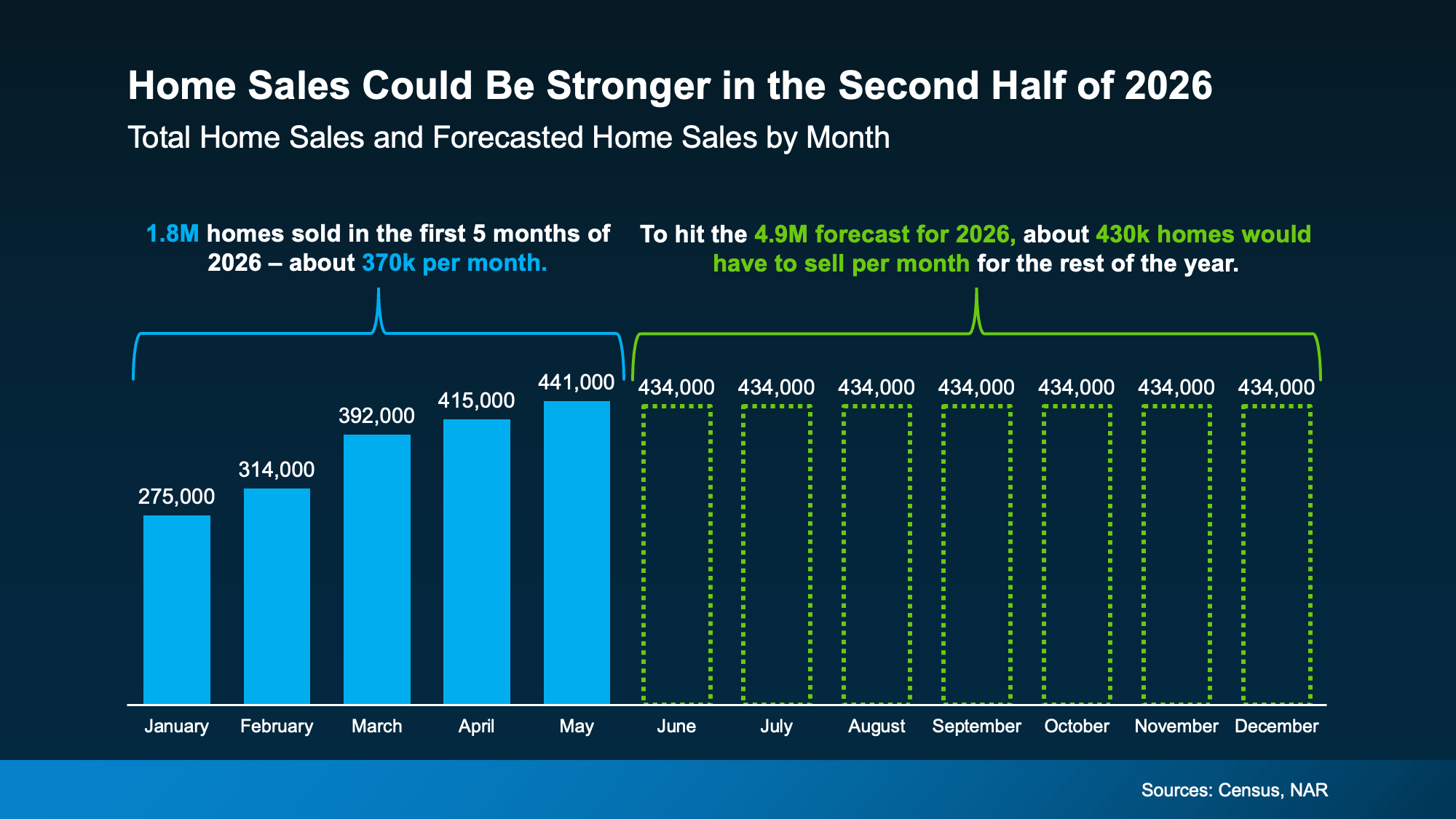

The source forecast shows that approximately 1.8 million homes sold during the 1st 5 months of 2026, averaging about 370,000 sales per month. To reach the forecast of approximately 4.9 million sales for the entire year, monthly sales would need to rise to roughly 430,000 for the remaining months.

That would require a stronger 2nd half than the beginning of the year. Improved affordability, greater economic confidence, and buyers becoming more comfortable with current conditions could all help increase activity.

Many people who postponed a move still have a reason to buy or sell. Growing families, job changes, retirement, marriage, divorce, inheritance, and relocation needs do not disappear because the market is uncertain.

If mortgage rates become more favorable, some of that delayed demand may return. The increase would probably be gradual, and the pace could vary substantially from one local market to another.

Buyers should monitor mortgage rates, available inventory, price reductions, seller concessions, and how long comparable homes remain on the market. These factors can help indicate whether buyers have meaningful negotiating leverage within a specific price range and community.

A buyer searching in Brandon or Riverview may encounter different inventory and new construction competition than someone searching in South Tampa, Carrollwood, Westchase, or Seminole Heights. The same is true when comparing St. Petersburg, Clearwater, Largo, Seminole, and Palm Harbor.

Buyers should also distinguish between single family homes, townhomes, and condominiums. Each property type may have different insurance requirements, association fees, maintenance responsibilities, financing considerations, and resale conditions.

A strong preapproval and a clear monthly budget can help buyers act confidently when the right property becomes available. It also helps prevent buyers from focusing on homes that do not fit their actual payment goals.

Sellers should pay close attention to competing listings, recent pending sales, buyer feedback, showing activity, and average market time. The number of homes for sale matters, but the condition and pricing of those homes are equally important.

Property preparation can have a meaningful effect on the result. Addressing visible maintenance issues, improving presentation, gathering permit and repair documentation, and making the home easy to show can help reduce buyer uncertainty.

Florida buyers may also ask detailed questions about the roof, HVAC system, electrical panel, plumbing, insurance history, flood zone, and wind mitigation features. Providing accurate information early can make the transaction smoother and help buyers evaluate the property with confidence.

Sellers should remain flexible without automatically accepting unfavorable terms. A well structured offer may include a strong price, reliable financing, reasonable inspection terms, sufficient escrow, and a closing timeline that fits the seller’s plans.

The Tampa Bay housing market is made up of many smaller markets. Conditions in Hillsborough County can differ from Pinellas County, and trends can change again when the analysis is narrowed to a city, neighborhood, property type, or price range.

A single family home in FishHawk may not compete with the same buyers as a downtown Tampa condominium. A St. Petersburg bungalow may respond differently from a Clearwater Beach condo or a newer Largo home.

That is why buyers and sellers should avoid making decisions based only on national headlines. Local sales data, current competition, property specific expenses, and personal financial goals provide a more useful foundation.

The 2nd half of 2026 may offer gradual improvement rather than a dramatic change. Mortgage rates could ease, national home prices are forecast to remain modestly positive, and home sales may gain momentum as more people move forward with delayed plans.

Buyers should not assume that waiting guarantees both a lower rate and a lower price. Sellers should not assume that national price growth guarantees their home will sell for any asking price.

The strongest decisions will come from evaluating current Tampa Bay market conditions alongside your personal goals, budget, property type, and timeline. We can help you review the local numbers and create a strategy for buying or selling in Hillsborough County, Pinellas County, and communities throughout the greater Tampa Bay area.