If you are receiving a tax refund this year, it may be more useful than you think. For many buyers, the biggest challenge is not wanting to buy a home. It is coming up with the money needed upfront.

That is where a refund can help. Even if it does not cover every cost, it can move you closer to your savings goal, strengthen your buying plan, or help reduce the amount you need to save before making an offer.

For buyers in the greater Tampa Bay area, every dollar matters because the full cost of buying includes more than the down payment. Property taxes, insurance, HOA fees, closing costs, prepaid expenses, and cash reserves can all affect what you need before closing.

A tax refund can arrive at a useful time for buyers who are already thinking about purchasing. If you have been saving gradually, a refund may help you reach the next step faster.

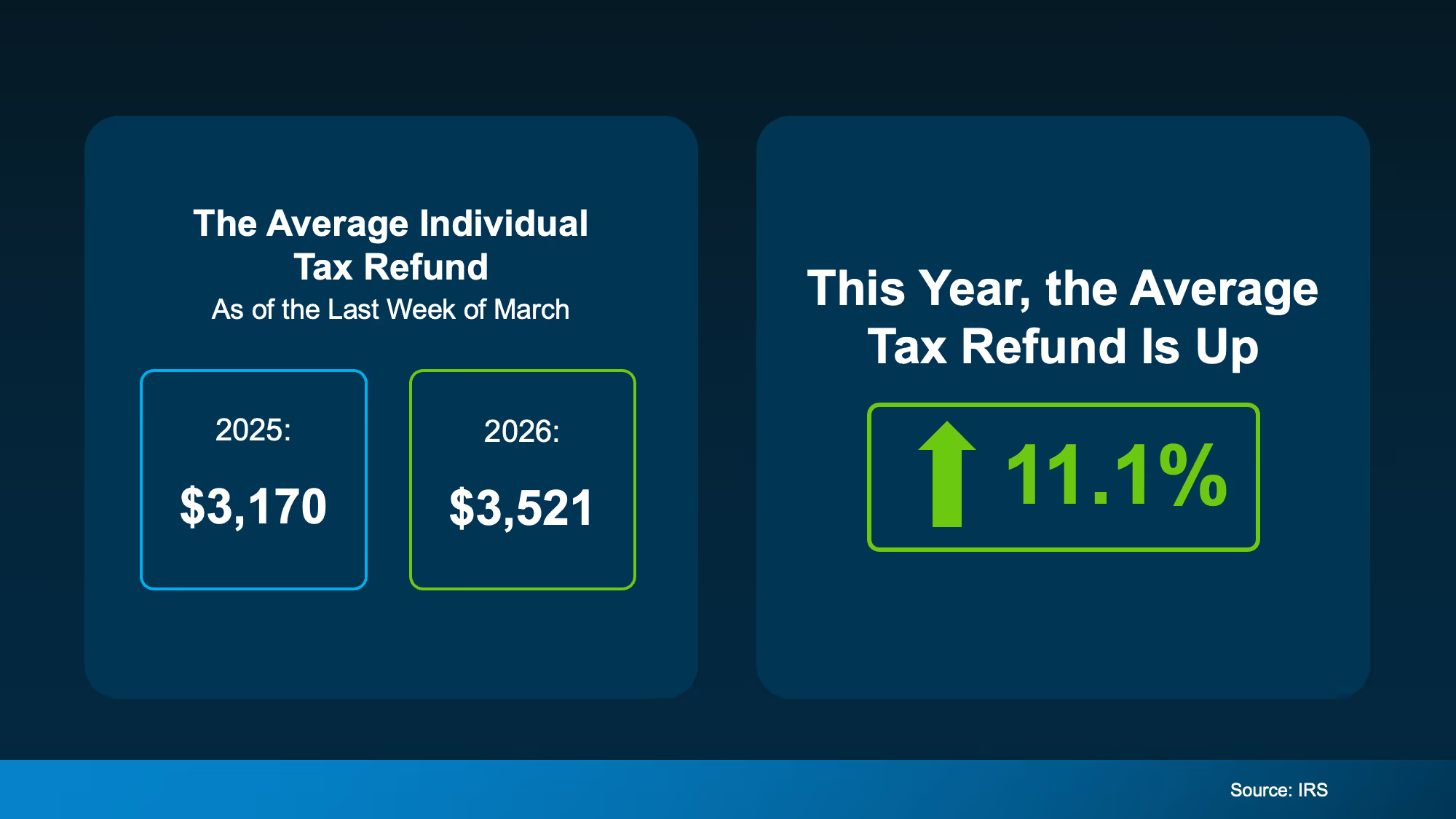

The graphic in the original article shows the average individual tax refund increasing compared with the prior year. Your actual refund may be higher or lower, but the point is simple. A lump sum can make a meaningful difference when you are building your home buying funds.

Instead of spending the refund without a plan, consider separating it into a dedicated home buying savings account. That can make it easier to track your progress and avoid mixing it with everyday spending.

One of the most common ways to use a tax refund is to put it toward the down payment. This can be especially helpful for first-time buyers who are trying to build savings while also managing rent, utilities, car payments, childcare, insurance, and other monthly expenses.

Many buyers are surprised to learn that they may not need 20% down to buy a home. Depending on the loan program, some buyers may qualify with a smaller down payment, while eligible VA or USDA buyers may have options that require $0 down.

That does not mean every buyer should put down the minimum. A larger down payment may reduce the loan amount, lower the monthly payment, or help with loan approval. The right amount depends on your budget, loan type, credit profile, and long-term goals.

A tax refund can also help with closing costs. These are the upfront costs involved in getting the loan and completing the purchase.

Closing costs often include lender fees, title-related costs, recording fees, prepaid interest, escrow deposits, property taxes, homeowners insurance, and other settlement charges. The exact amount can vary based on the home price, loan type, lender, property location, insurance, and whether the seller is contributing toward your costs.

For Tampa Bay buyers, this part of the budget deserves close attention. Insurance premiums, property taxes, HOA fees, condo fees, and escrow requirements can vary significantly between Tampa, Riverview, Brandon, St. Petersburg, Clearwater, Largo, Westchase, FishHawk, and surrounding areas.

Using a refund toward closing costs may help reduce the amount of cash you need to bring to closing. It can also make the purchase feel more manageable when combined with seller credits, lender credits, or down payment assistance if you qualify.

Another option is using part of your refund to lower your mortgage rate through discount points or a buydown. This means paying more upfront in exchange for a lower monthly payment.

This strategy can make sense if the monthly savings are meaningful and you expect to stay in the home long enough to benefit from the lower payment. It may not make sense if you plan to sell or refinance soon, because you may not recoup the upfront cost.

Before using your refund this way, ask your lender to show the difference side by side. You want to compare the upfront cost, monthly savings, break-even point, total interest, and how long you realistically expect to keep the loan.

A lower rate can help affordability, but it is not automatically the best use of your money. Sometimes keeping extra cash available for reserves, repairs, moving costs, or emergency savings may be the smarter choice.

Buying a home takes planning beyond the closing table. After you move in, you may need money for repairs, furniture, appliances, utilities, maintenance, landscaping, or unexpected expenses.

That is why some buyers may benefit from keeping part of their refund as reserves. Having extra money left after closing can create breathing room and reduce stress during the first few months of homeownership.

This is especially important in Florida, where insurance, weather-related maintenance, roof age, AC condition, and property upkeep can all affect your long-term budget. A refund can help you buy, but it can also help you stay financially comfortable after you buy.

The best use of your tax refund depends on where you are in the buying process. A buyer who is short on down payment funds may use it differently than a buyer who already has the down payment but needs help with closing costs or reserves.

Start by getting pre-approved and asking your lender for an estimated cash to close. That estimate can help you understand how much money you may need for the down payment, closing costs, prepaid expenses, escrow deposits, and other adjustments.

Once you see the numbers, you can decide whether your refund should go toward the down payment, closing costs, rate buydown, debt reduction, or savings. The goal is not just to use the money. It is to use it in the way that gives you the strongest path forward.

A tax refund can be a practical tool for home buyers. It may help with the down payment, closing costs, a mortgage rate buydown, or reserves after closing.

For Tampa Bay buyers, the smartest move is to connect the refund to a clear plan. Understand your loan options, know your estimated cash to close, and make sure you are budgeting for the full cost of ownership.

If buying a home is on your radar, do not overlook your refund. Used wisely, it could help you move from “almost ready” to ready with a stronger, more confident plan.