Many buyers assume they need 20% down before they can buy a home. That belief keeps a lot of people on the sidelines longer than necessary, especially first-time buyers who are already trying to balance savings, rent, insurance costs, and everyday expenses.

In the Tampa Bay area, where home prices and monthly payments can vary widely by neighborhood, it is easy to feel like the savings goal is too far away. But the truth is, most first-time buyers do not put 20% down. There are several loan options and assistance programs that may help qualified buyers purchase a home with much less upfront.

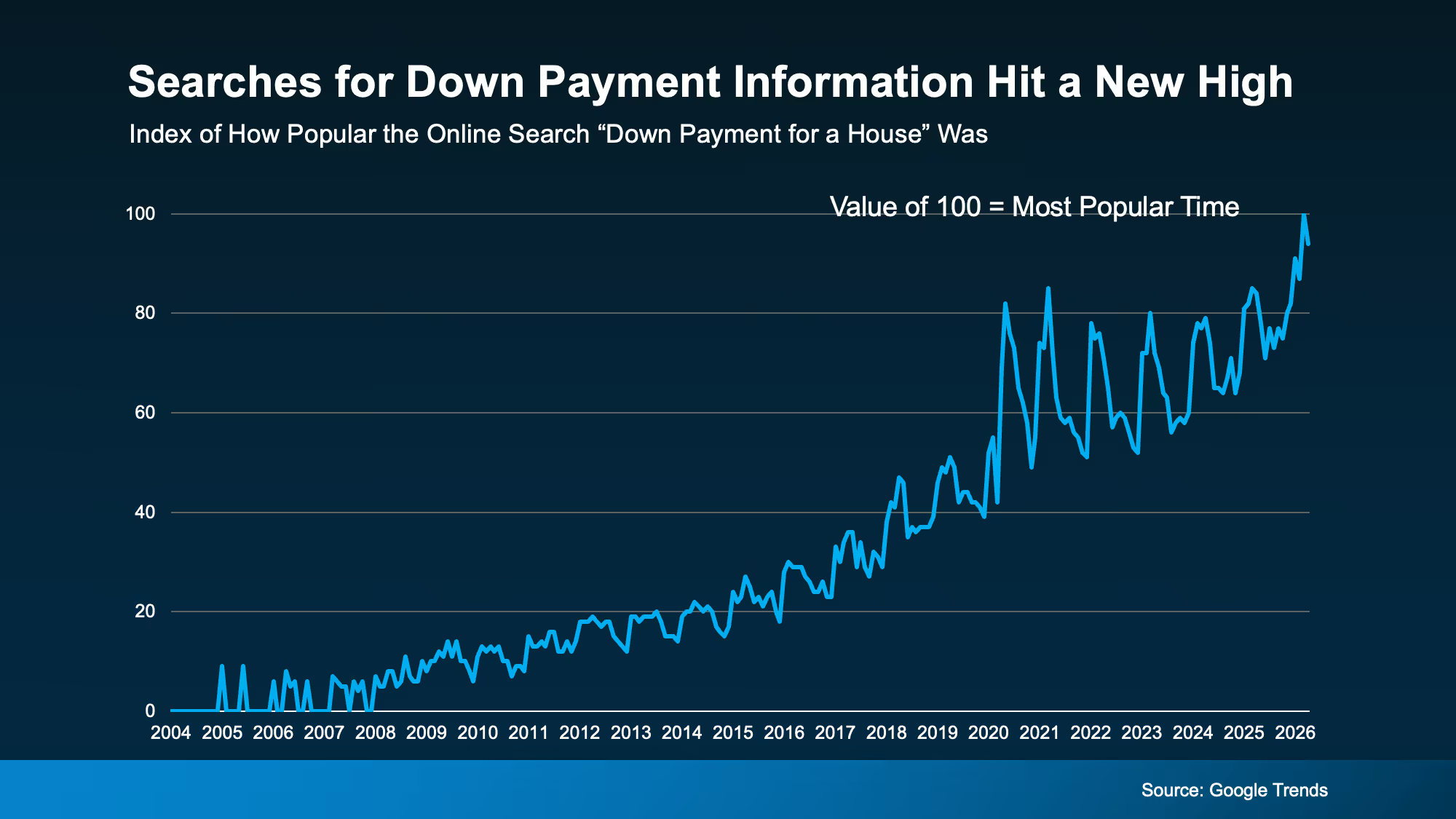

A lot of buyers are trying to figure out how much money they really need to save before making a move. That makes sense because the down payment is one of the first numbers people think about when they start planning to buy.

The problem is that many buyers get stuck on the wrong number. They hear 20% so often that they assume it is required, even though that is not the case for many loan programs.

A larger down payment can have benefits. It may reduce your loan amount, lower your monthly payment, and help you avoid certain costs depending on the loan type. But that does not mean 20% is the only path to homeownership

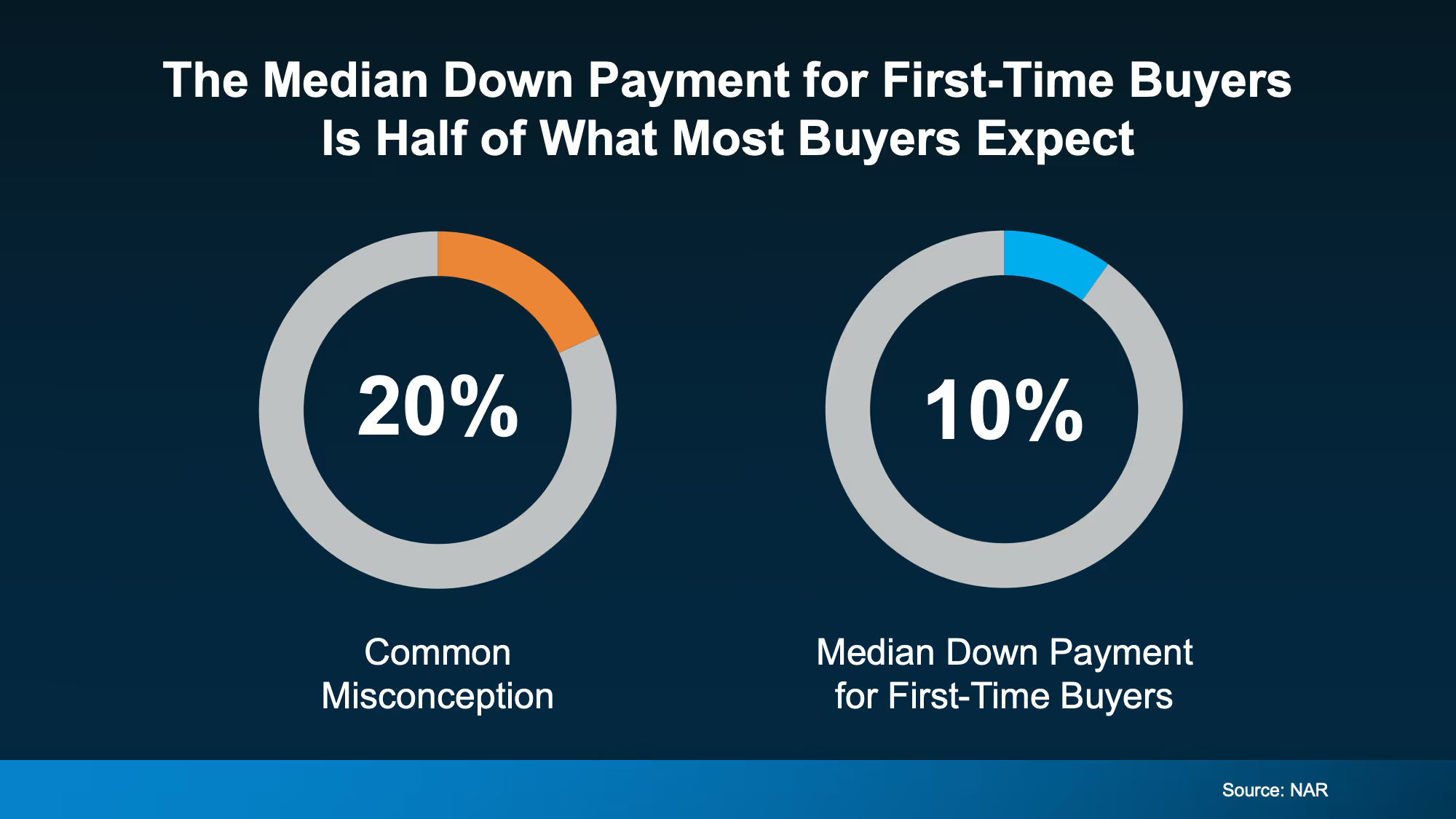

The idea that every buyer needs 20% down is one of the biggest misconceptions in real estate. Unless your lender tells you that your specific loan situation requires it, you may have options that require far less.

For example, FHA loans may allow qualified buyers to purchase with 3.5% down. Conventional loan programs may offer low down payment options for certain buyers. VA loans may offer 0% down for eligible Veterans, active-duty service members, and qualifying surviving spouses.

That can make a major difference for buyers in Hillsborough County and Pinellas County. Instead of waiting years to save 20%, some buyers may be able to start exploring their options sooner with a more realistic savings target.

Many first-time buyers put down much less than people expect. The uploaded article notes that the median down payment for first-time homebuyers is 10%, which is half of the 20% number many buyers think they need.

That does not mean 10% is required either. It simply shows that the typical first-time buyer is not necessarily waiting until they have 20% saved.

For someone buying a home in Tampa, Brandon, Riverview, St. Petersburg, Largo, Clearwater, or nearby areas, this can change the planning conversation. Instead of asking, “How long will it take me to save 20%?” the better question is, “What loan options fit my credit, income, savings, and monthly payment goals?”

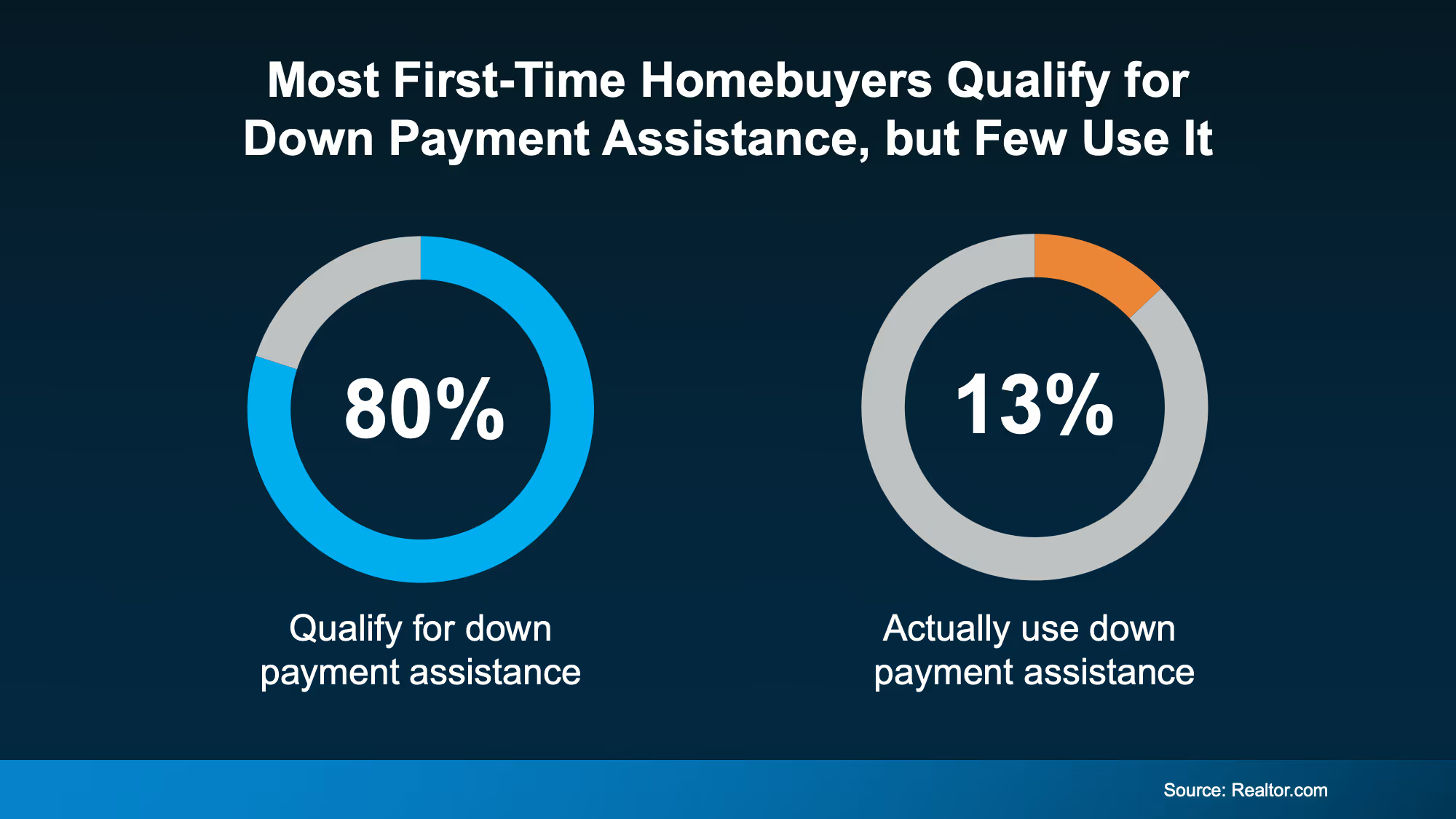

Down payment assistance can be another major piece of the puzzle. These programs are designed to help qualified buyers cover part of their down payment or closing costs, which may reduce the amount they need to bring to the table.

The challenge is that many buyers do not know these programs exist, or they assume they will not qualify. That can cause people to delay buying without ever checking whether help is available.

Programs vary by location, income, occupation, loan type, property type, and buyer status. Some are geared toward first-time buyers, while others may be available to repeat buyers, military buyers, or buyers in certain income ranges.

Down payment assistance can be helpful, but buyers should understand the details before building a plan around it. Not every program works the same way, and not every property or buyer will qualify.

Some programs may have income limits, purchase price limits, education requirements, repayment rules, or restrictions on where the home is located. Others may be structured as grants, forgivable loans, deferred loans, or second mortgages.

That is why it is important to work with a lender who understands the programs available in Florida and can explain the real numbers clearly. The goal is not just to qualify for assistance. The goal is to make sure the overall payment and long-term terms still make sense.

The down payment is only one part of the cash needed to buy a home. Buyers also need to plan for closing costs, inspections, appraisal fees, prepaid taxes, homeowners insurance, possible flood insurance, moving expenses, and emergency reserves.

In Florida, closing costs can vary depending on the loan type, purchase price, county, title charges, lender fees, and contract terms. Some buyers may also be able to negotiate seller credits, especially when a home has been on the market longer or the seller is motivated.

This is where local strategy matters. A buyer who only focuses on the down payment may overlook other costs that affect affordability. A buyer who looks at the full picture can make a stronger and more realistic plan.

The first step is to get clear on what you can comfortably afford each month. Your down payment affects the loan amount, but your monthly payment is what you will live with after closing.

Next, talk with a lender about loan programs that fit your situation. Ask about FHA, conventional, VA, USDA, and any Florida or local assistance programs that may apply.

Then compare your options carefully. Sometimes putting more money down makes sense. Other times, keeping more cash available for repairs, furniture, moving costs, or reserves may be the smarter move.

Most first-time buyers do not put 20% down, and many do not need to. If you have been waiting because you thought 20% was required, your timeline may be longer than it needs to be.

That does not mean every buyer should rush into the market with the lowest down payment possible. It means you should understand your real options before deciding whether buying is out of reach.

For Tampa Bay buyers, the right plan starts with knowing your loan options, checking whether assistance may be available, and reviewing the full cost of buying. Once you understand the numbers, you may find that homeownership is more realistic than you thought.