Renting can feel like the easier choice right now. With higher home prices, mortgage rates, insurance costs, and the upfront cash needed to buy, it is understandable why many people in the Tampa Bay area are asking whether homeownership still makes sense.

For some people, renting is the right move for the season they are in. It can offer flexibility, fewer maintenance responsibilities, and lower upfront costs. But if you are deciding whether to keep renting or start planning to buy, there is one part of the conversation that deserves more attention: what each option does for your future.

Renting can be practical, especially if you are unsure how long you will stay in one place or you are still building your savings. You may not have to worry about repairs, property taxes, homeowners insurance, or ongoing maintenance the same way an owner does.

That flexibility has value. For someone relocating, changing jobs, rebuilding credit, saving for a down payment, or waiting for more financial stability, renting can be a smart temporary step.

The challenge is that rent does not create ownership. Each monthly payment gives you a place to live for that month, but it does not build equity, increase your ownership stake, or create an asset you can use later. Over time, that can become the biggest tradeoff.

When you own a home, your monthly payment is not just paying for a roof over your head. Part of that payment helps reduce what you owe, and as your loan balance goes down, your ownership stake can grow.

That ownership stake is called equity. Equity is the difference between what your home is worth and what you still owe on it. In markets like Hillsborough County and Pinellas County, where many homeowners have benefited from long-term appreciation, equity can become one of the most important financial advantages of owning.

Home values will always move with the market, and there are no guarantees. But historically, homeownership has been one of the most common ways households build wealth over time because it combines shelter with a long-term asset.

The difference between renters and homeowners is not just about monthly housing costs. It is also about whether those payments are helping build something you may be able to use later.

For a homeowner, equity can eventually support future goals. It may help with a move-up purchase, renovations, debt consolidation, investment opportunities, retirement planning, or simply creating more financial stability. For a renter, the monthly payment provides housing, but the long-term ownership benefit goes to the landlord.

That is why the rent vs. buy decision is not only about what feels cheaper today. It is also about what position you want to be in 5, 10, or 20 years from now.

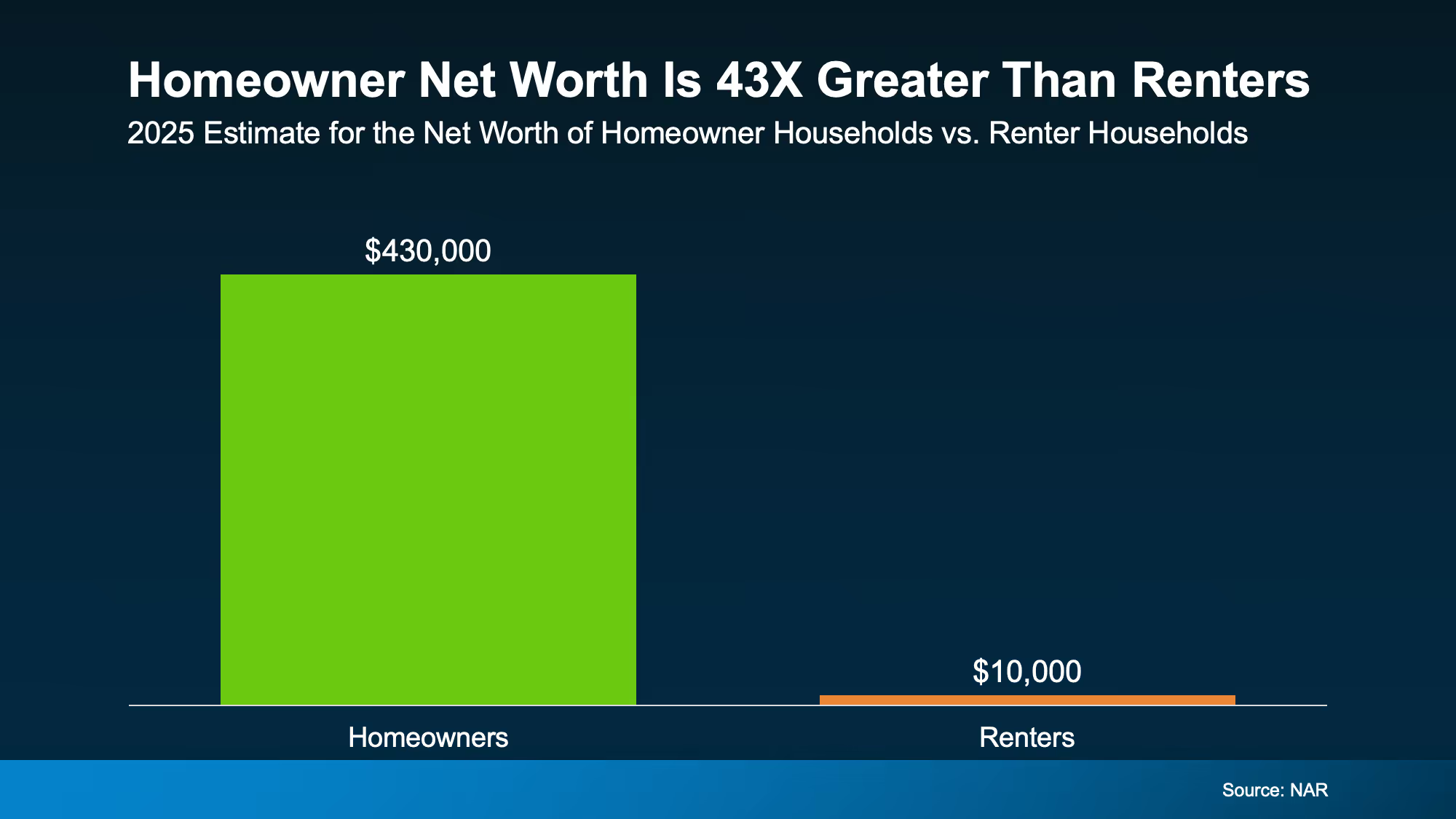

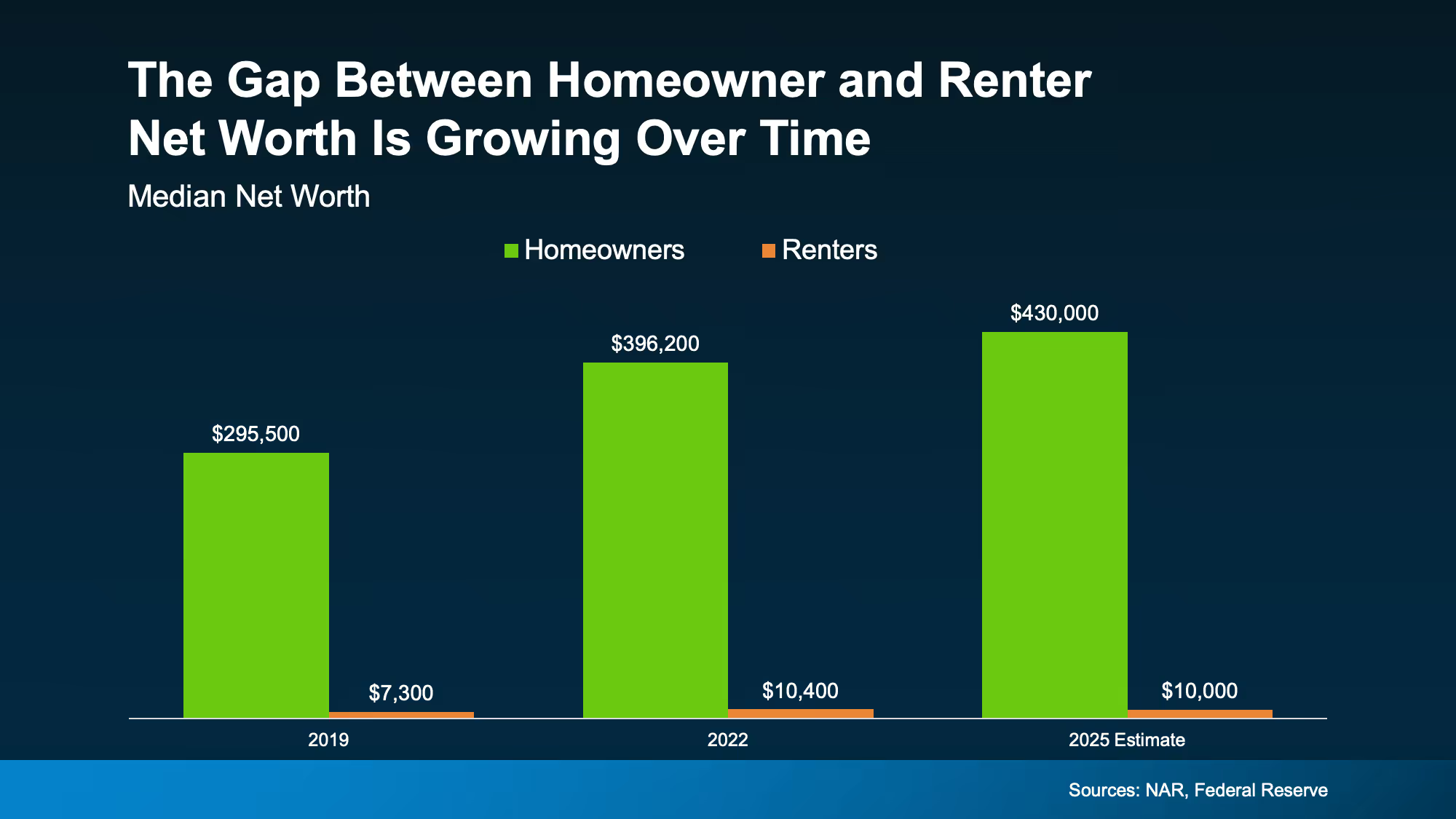

One of the biggest reasons people continue to pursue homeownership is the long-term wealth gap between owners and renters. The visual in this article shows how homeowner net worth has continued to pull away from renter net worth over time.

That does not mean buying is automatically the right decision for everyone today. It does mean the long-term impact of ownership is worth considering, especially if you plan to stay in the area and your finances can support the purchase.

Even when home prices cool or grow more slowly, homeowners may still continue building equity by paying down their mortgage. That is a major difference from renting, where monthly payments usually rise over time but do not create ownership for the tenant.

The right answer depends on your budget, timeline, savings, credit, lifestyle, and comfort level with responsibility. Buying a home can be a great long-term move, but it should not stretch you beyond what is realistic.

In the greater Tampa Bay area, buyers also need to think through property taxes, homeowners insurance, flood zones, HOA fees, commute patterns, school zones, and future resale potential. A home that looks affordable on paper may feel very different once all ownership costs are included.

That is why the first step is not simply looking at homes online. The better first step is understanding your numbers, comparing realistic monthly costs, and deciding whether the benefits of ownership outweigh the flexibility of renting for your situation.

Start with your timeline. If you expect to move again soon, renting may make more sense because buying and selling both come with costs.

Next, look at your cash position. You will need to consider your down payment, closing costs, inspection costs, moving expenses, emergency reserves, and any repairs or updates the home may need after closing.

Then compare the long-term picture. If you plan to stay put and your payment is manageable, buying may give you the chance to build equity instead of continuing to pay rent without ownership.

Renting may feel easier today, and for some people, it is the right short-term choice. But over time, renting can come with a hidden cost because your payments are not building equity for your future.

Buying a home is a bigger commitment, and it should be approached carefully. But when the numbers work and the timing is right, homeownership can help you build wealth, create stability, and put your monthly housing payment to work in a more meaningful way.

Whether you are ready now or just starting to plan, the goal is to know your options clearly. Once you understand the numbers, the market, and the long-term tradeoffs, you can make a decision with more confidence.