Inflation affects more than groceries, gas, utilities, and insurance.

It can also affect mortgage rates, monthly payments, buyer confidence, and the overall cost of owning a home. That is why inflation matters so much for anyone thinking about buying in the greater Tampa Bay area.

When inflation rises, the cost of everyday life goes up. For buyers, that can make it harder to save for a down payment, cover closing costs, qualify for financing, or feel comfortable with a monthly housing payment.

And in Florida, where buyers are also watching insurance premiums, property taxes, HOA fees, CDD fees, flood zones, and maintenance costs, inflation can make affordability feel even tighter.

One of the main reasons inflation matters in real estate is its connection to interest rates.

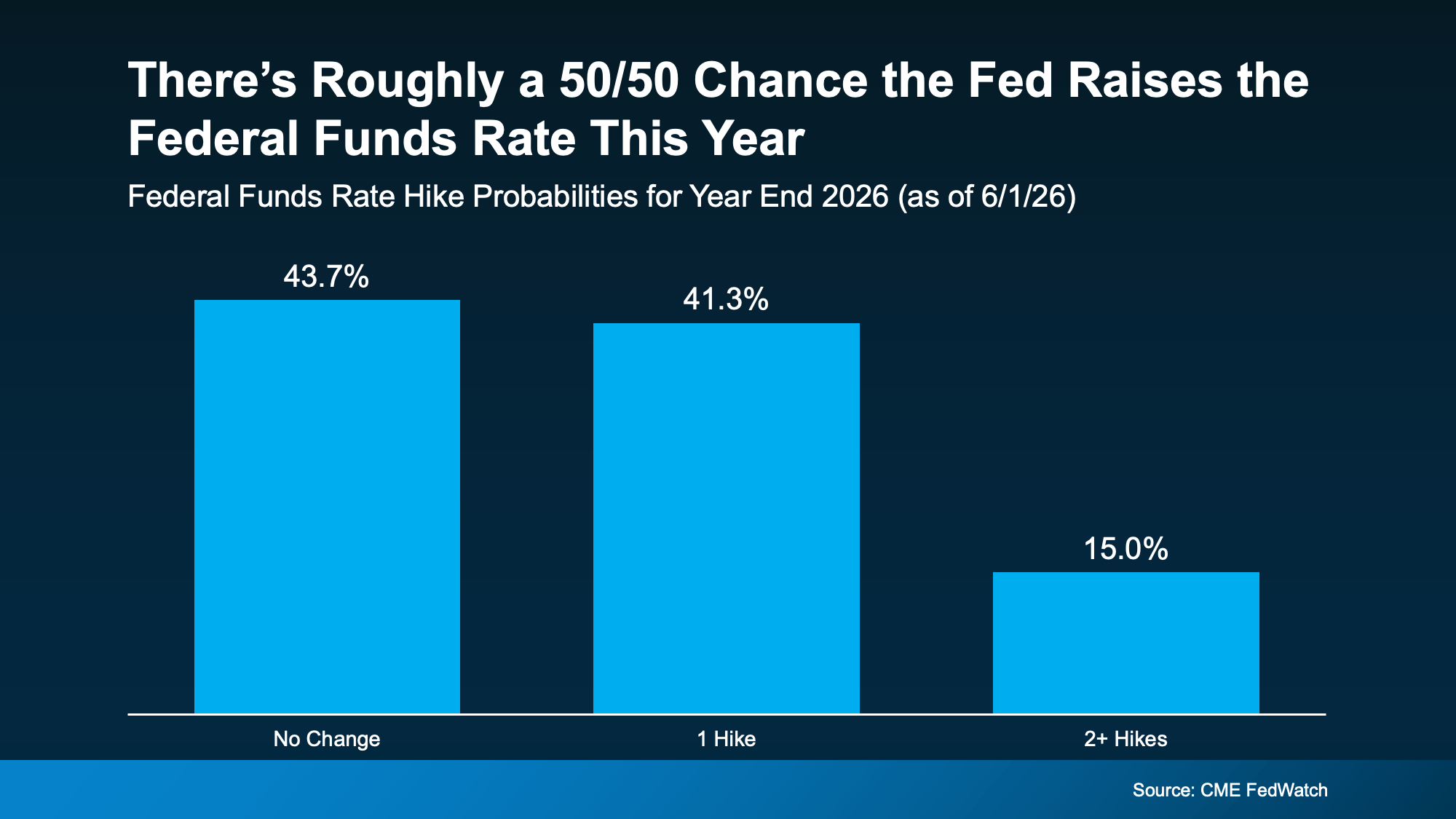

The Federal Reserve does not directly set mortgage rates, but its decisions can influence the broader rate environment. When inflation stays higher than desired, the Fed may keep rates elevated longer or consider raising rates to help slow spending and cool inflation.

That can affect what buyers pay for a mortgage.

For buyers in Tampa, Riverview, Brandon, St. Petersburg, Clearwater, Largo, Seminole, Westchase, and surrounding communities, even a small change in mortgage rates can have a major impact on purchasing power. A higher rate can reduce the price range a buyer can comfortably afford, while a lower rate can bring more homes back within reach.

This is why waiting for rates to fall can be risky. Rates may improve later, but they may also stay higher longer than expected.

Not all inflation readings tell the same story.

One measure often discussed is PCE, which stands for Personal Consumption Expenditures Price Index. It tracks how much people are paying for goods and services compared to a year earlier.

Another measure is core PCE, which removes food and energy because those prices can move sharply from month to month. The Fed often watches core PCE closely because it can give a clearer picture of underlying inflation trends.

That difference matters for the housing market.

If inflation is rising mostly because of temporary energy price swings, the long-term impact may be different than if inflation is rising broadly across the economy. But until inflation clearly cools, mortgage rates may remain a challenge for buyers.

Higher mortgage rates make buying harder, but they do not automatically make buying a bad decision.

The right answer depends on your budget, timeline, income, debt, savings, loan type, and how long you plan to own the home. For some buyers, it may make sense to wait. For others, buying now with the right strategy may still be the better move.

That is especially true if waiting only creates a different problem.

If rates fall later, more buyers may re-enter the market. That could increase competition, reduce negotiation leverage, and make the best homes harder to secure. If rates stay elevated, waiting may not create the affordability improvement buyers were hoping for.

The goal is not to predict the perfect moment. The goal is to understand your numbers and make a decision that works in the market we actually have.

Rising inflation and elevated mortgage rates can make the market feel uncomfortable, but that does not mean the housing market is crashing.

Today’s market is very different from the conditions that led to 2008. Lending standards are stronger, most homeowners have more equity, and there is not a flood of distressed properties hitting the market.

That does not mean every market is strong or every home will sell quickly.

It means today’s challenge is largely affordability, not a widespread collapse in housing fundamentals. Buyers are cautious because payments are higher. Sellers are adjusting because buyers have become more selective.

In Tampa Bay, the difference can vary by location, property type, condition, and price range. A well-priced single-family home in good condition may perform very differently than an overpriced condo with rising fees or a home needing major updates.

When inflation and rates are high, buyers need a more careful plan.

That starts with getting clear on the full monthly payment, not just the purchase price. Buyers should review principal, interest, taxes, insurance, HOA fees, CDD fees, flood insurance, utilities, maintenance, and any other recurring costs before making an offer.

It may also help to ask your lender about different loan options.

Depending on your situation, you may want to compare fixed-rate loans, adjustable-rate mortgages, temporary rate buydowns, permanent rate buydowns, seller credits, down payment assistance, or first-time buyer programs. Each option has pros and cons, so the details matter.

Buyers should also pay close attention to negotiation opportunities. In a slower market, some sellers may be more open to closing cost credits, repairs, price adjustments, or other terms that help make the purchase more manageable.

Inflation also affects sellers.

When buyers are dealing with higher costs and higher rates, they tend to be more selective. They may compare homes more carefully, negotiate harder, and move slowly if a home feels overpriced.

That means sellers should not assume buyers will overlook condition, pricing, insurance concerns, or needed repairs.

A strong listing strategy should account for the current affordability pressure buyers are facing. That may include pricing realistically, preparing the home well, reviewing competing listings, and understanding what buyers in your specific price range are responding to.

In today’s market, the right price and presentation can make a major difference.

Inflation matters because it can keep mortgage rates elevated, reduce buyer purchasing power, and make monthly payments harder to manage.

But higher inflation does not mean buying or selling is impossible.

For buyers, the key is to understand the full cost of ownership and use the right financing and negotiation strategy. For sellers, the key is to recognize how affordability affects buyer behavior and price the home for today’s market.

The Tampa Bay housing market is not one-size-fits-all.

Your best move depends on your goals, your numbers, and the local conditions affecting your specific home, neighborhood, and price range.