Homeowners insurance is a critical part of your housing budget — often as significant as your mortgage, taxes, and maintenance costs. In Florida, where weather risk and property requirements vary widely, understanding insurance costs ahead of time can prevent payment shock later.

Insurance protects your home, belongings, and liability exposure. Premiums can differ dramatically based on location, roof age, construction type, and weather exposure. Florida buyers need to factor these costs into affordability assessments before finalizing a purchase.

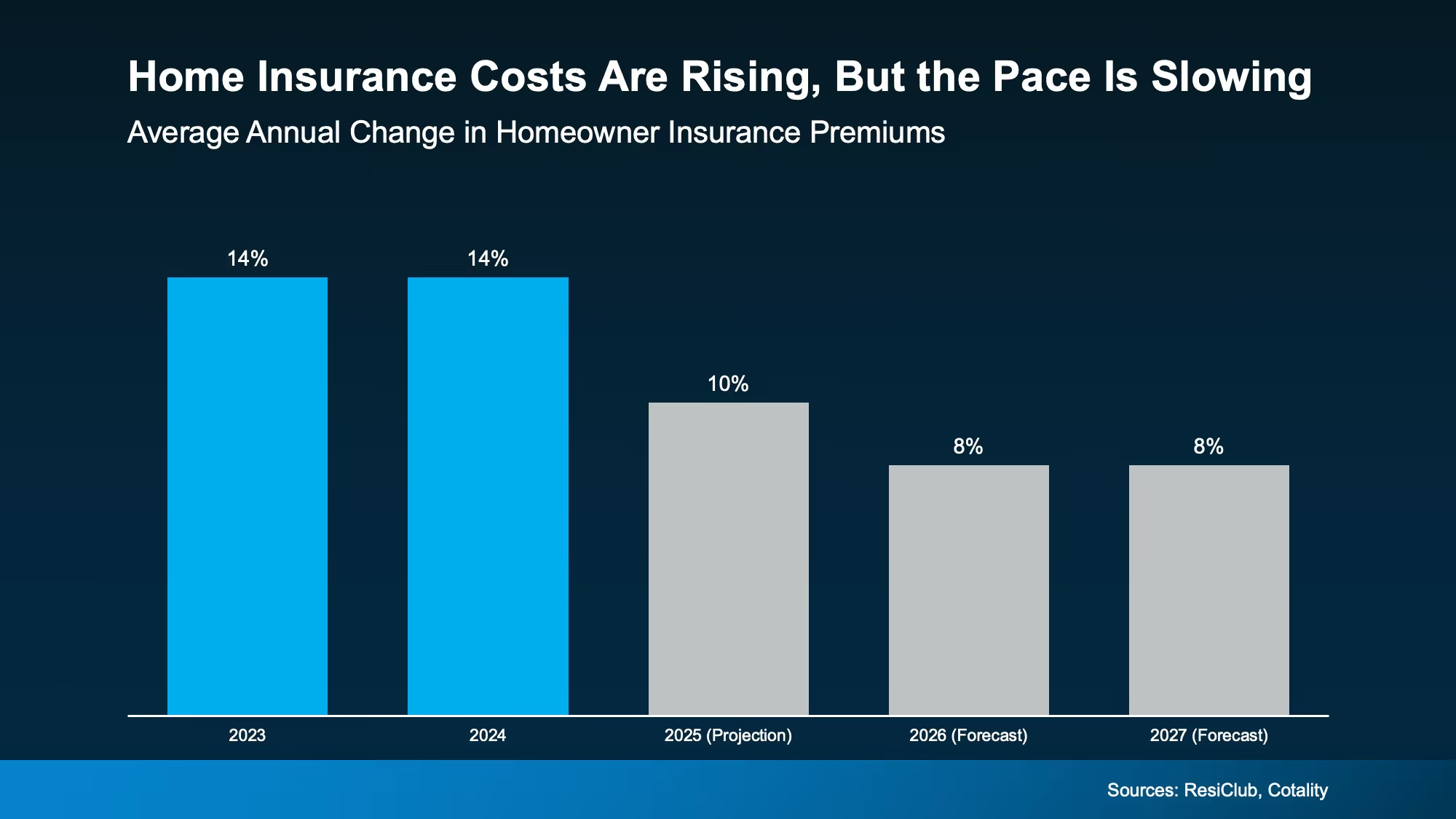

Rising rebuilding costs, labor shortages, and increased severe weather events have pushed insurance costs higher in recent years. While there are signs the pace of increases may moderate, budgeting realistically remains essential.

1. Get early, property-specific quotes — Don’t wait until after inspections or contract execution.

2. Understand roof and inspection requirements — Wind mitigation and four-point inspections can affect eligibility and pricing.

3. Integrate premiums into your payment calculations — Whether escrowed or paid directly, increases can affect your monthly budget.

4. Build a cushion into your affordability target — Stretching to the max leaves no room for increases at renewal.

Comparing quotes from multiple carriers, documenting risk-reducing upgrades (new roof, storm shutters), asking about discounts, and reviewing coverage limits carefully can help you balance cost with protection.

Key Takeaway: Treat insurance planning as an early step in your homebuying process — not an afterthought at closing.