Saving for a down payment can feel like the biggest obstacle between you & buying a home. That is especially true in the greater Tampa Bay area, where buyers are also thinking about mortgage rates, insurance, taxes, HOA fees, flood zones, & the monthly payment.

But the amount buyers are putting down has actually come down from recent highs. That does not mean buying is easy, but it does mean some buyers may have more options than they realize.

If you are looking at homes in Tampa, St. Petersburg, Clearwater, Brandon, Riverview, Carrollwood, Westchase, Largo, Dunedin, Palm Harbor, Seminole, or Safety Harbor, it is worth understanding how today’s down payment options work before assuming you need a massive amount of cash to get started.

According to the data in the article, the typical buyer put down about $23,400 in early 2026. That was roughly $5,000 lower than the year before, which represents a 19% drop year over year.

The chart also shows that down payments are now at their lowest point since 2021.

That matters because many buyers still believe they need 20% down to buy a home. A 20% down payment can be helpful, especially if you want to avoid private mortgage insurance on a conventional loan, but it is not the only path to homeownership.

For many Tampa Bay buyers, the more important question is not, “Do I have 20% down?” It is, “What loan programs, assistance options, monthly payment, & cash-to-close strategy actually fit my situation?”

There are a few reasons down payments have gotten smaller. One major factor is that the market is more balanced than it was during the intense competition of 2020 & 2021. When buyers are not fighting through the same level of bidding wars, they may feel less pressure to put down a larger amount just to make their offer stand out.

Another factor is slower home price growth in many markets. Since a down payment is tied to the purchase price, more moderate pricing can affect how much cash a buyer needs to bring to closing.

Loan choice also plays a major role. More buyers are using loan programs with lower down payment requirements, including FHA & VA loans. The article notes that FHA loans have represented more than 24% of purchase mortgages for 5 straight quarters, while VA loans recently reached their highest share in more than 10 years.

The 20% down payment idea is one of the most common misunderstandings in real estate. Some buyers hear that number & assume they are years away from buying, even though they may qualify with much less.

FHA loans are commonly used by buyers who want a lower down payment option. VA loans can be especially powerful for eligible veterans, active-duty service members, & qualifying surviving spouses because they may allow $0 down. Conventional loans may also offer lower down payment options depending on the buyer, the property, & the lender’s guidelines.

The right option depends on your credit, income, debt, savings, purchase price, property type, & long-term plans. A buyer looking for a condo in St. Petersburg may need a different strategy than a buyer looking for a single-family home in Riverview, Brandon, or Palm Harbor.

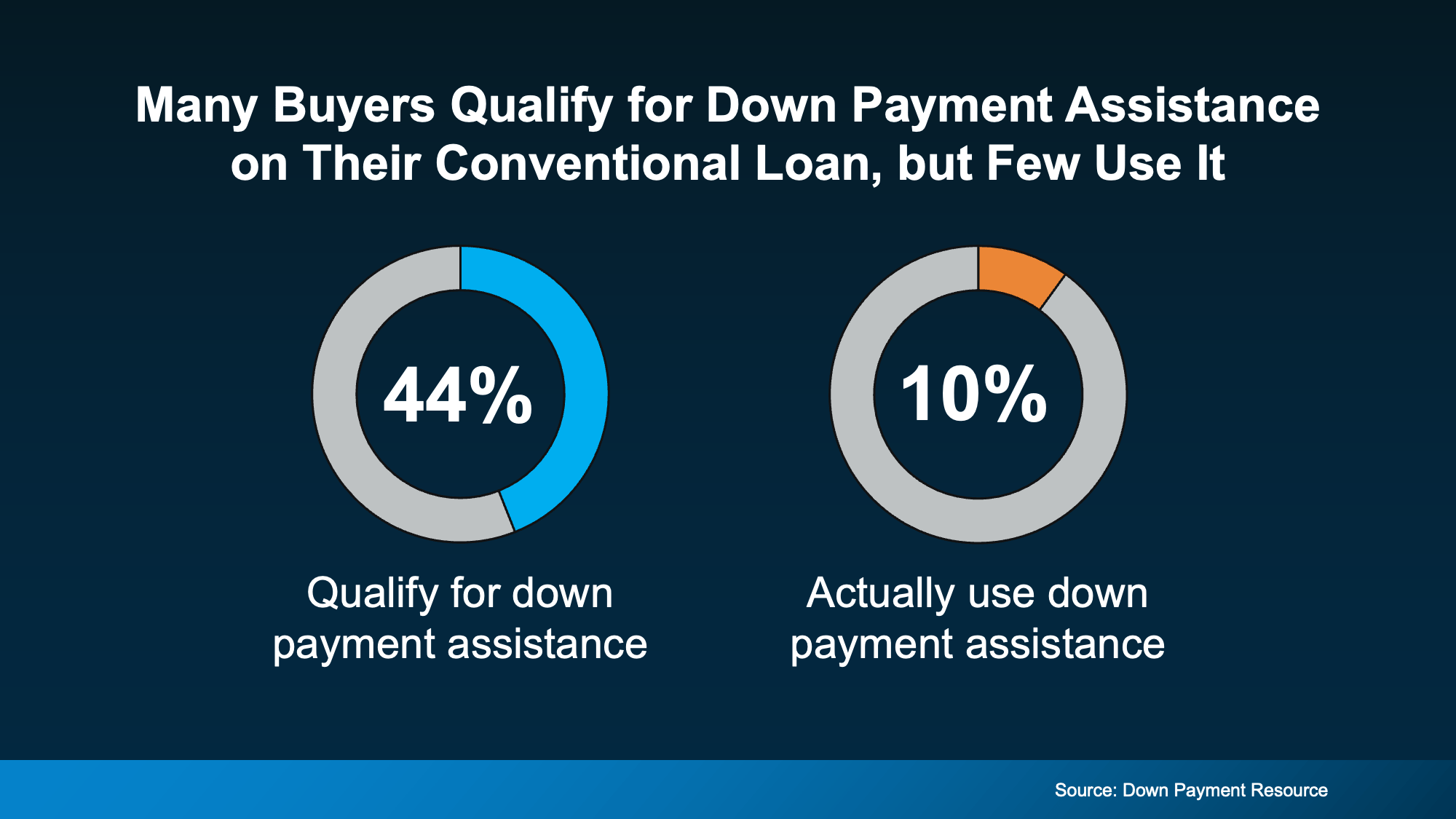

Down payment assistance is one of the most overlooked tools for buyers. The article points to research showing that nearly 44% of recent buyers in the 10 largest U.S. metros qualified for a down payment assistance program, but only 10% actually used one.

That gap is important. It suggests many buyers may be missing out simply because they do not know what is available, do not ask early enough, or are working with someone who does not regularly look at assistance options.

In Florida, buyers should ask about state-level assistance, local housing finance authority options, & city or county programs. Some programs are focused on first-time buyers, while others may have broader eligibility. Funding availability, income limits, purchase price limits, approved lender rules, & repayment terms can change, so this is something to review early in the process.

For Tampa Bay buyers, assistance options may vary depending on whether the property is in Hillsborough County, Pinellas County, the City of Tampa, or another municipality. That location detail matters because a buyer may qualify for one program in one area but not another.

This is why it helps to start with a lender who understands Florida buyer assistance programs. It is also helpful to work with a real estate brokerage that knows how to structure offers around financing, closing costs, seller credits, inspections, insurance, & appraisal risk.

The goal is not just to find a program. The goal is to make sure the full purchase plan works from contract to closing.

The article also explains that family help is becoming more common. Research cited in the article shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support often goes toward the down payment, closing costs, or helping the buyer qualify. For some buyers, even a modest gift can make the difference between waiting another year & being able to move forward now.

Gift funds need to be handled correctly. Lenders usually require documentation, & the money must come from an acceptable source under the loan guidelines. Before receiving or moving money, buyers should speak with their lender so the funds are documented the right way.

A lower down payment can help you buy sooner, but it does not remove the need for a strong plan. Buyers still need to understand the full cash needed to close, including escrow deposit, inspections, appraisal, loan costs, prepaid taxes, prepaid insurance, title charges, & other closing expenses.

You also need to think about the monthly payment. In Florida, insurance & taxes can have a major impact on affordability, especially when comparing homes in different parts of Hillsborough County & Pinellas County.

The strongest buyers are not always the ones putting the most money down. Often, they are the ones who are fully prepared, properly pre-approved, realistic about their price range, & clear on which costs they can negotiate.

If you have been waiting because you thought you needed a huge down payment, it may be time to recheck your options. Between lower down payment loan programs, assistance programs, seller credits, & possible gift funds, there may be more ways forward than you expected.

This does not mean every buyer should rush. It means you should get clear numbers before making a decision. A lender can help you compare loan options, while we can help you understand what is realistic in the neighborhoods, price ranges, & property types you are considering.

A first-time buyer in Tampa may have a different path than a move-up buyer in Clearwater or a veteran using VA financing in Brandon. The right strategy depends on your specific finances & the local market you are entering.

Down payments are smaller than they have been in several years, which may open the door for more buyers. The typical buyer put down about $23,400 in early 2026, down roughly $5,000 from the year before.

Buyers may be putting less down because the market is more balanced, price growth has cooled, & more people are using loan programs with lower down payment requirements. Down payment assistance & family gift funds can also make a meaningful difference when used correctly.

Before assuming you cannot buy, take time to review your options. For Tampa Bay buyers, the best first step is understanding your loan choices, assistance opportunities, cash needed to close, & realistic monthly payment before you start shopping seriously.