A common misconception is that you need “excellent” credit to qualify for a mortgage. That belief keeps many renters stuck, even when they may be closer than they think.

The truth is more nuanced: lenders look at credit score, but also review income, debt to income ratio, cash reserves, and overall credit history. There is not one universal score that guarantees approval or denial.

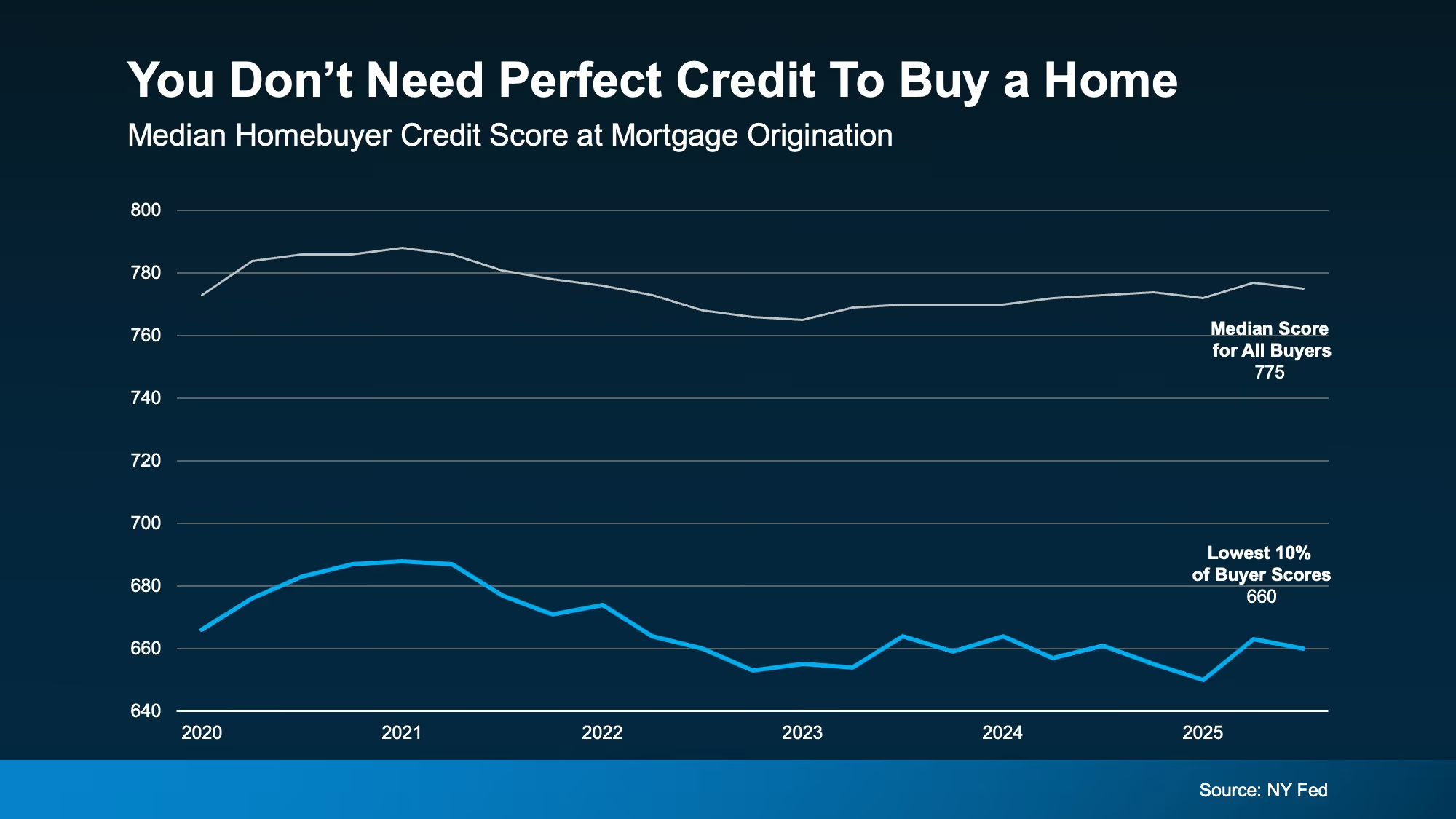

Many buyers do have strong credit scores. But that does not mean everyone who bought a home had a top tier score.

Some recent buyers qualified with scores well below the typical median, including a meaningful share in the 600s.

Different lenders have different risk tolerances and different program options. Two buyers with the same score can get different results depending on:

This is why an online “minimum score” answer is often misleading. The right next step is an actual review with a lender who can run scenarios.

If monthly debt payments are high relative to income, approval becomes harder even with a decent score. Paying down revolving balances can improve the score and the ratio at the same time.

Utilization can move a score quickly. Getting balances below key thresholds can create meaningful improvement without waiting months.

Late payments and collections usually hurt more than people expect. Consistent on time payment history is one of the strongest positive factors.

For Tampa Bay buyers, the monthly payment is not just principal and interest. Taxes, homeowners insurance, flood insurance in certain zones, and HOA fees can change affordability dramatically. Qualification is tied to that full payment, not just the home price.

Pull your credit reports and make sure the information is accurate. Errors happen, and you cannot fix what you do not see.

A lender can often tell you what is realistic with your current score and what small changes could move you into a stronger tier.

The goal is not only approval. It is a sustainable payment with enough cash left for moving costs, reserves, and homeownership expenses.