An adjustable-rate mortgage, often called an ARM, is a home loan with an interest rate that can change over time. It usually starts with an initial fixed period where the rate stays the same, and then the rate can adjust on a set schedule after that.

That is different from a fixed-rate mortgage, where the interest rate stays the same for the life of the loan. With a fixed-rate mortgage, the principal & interest portion of the payment is more predictable. Taxes, insurance, HOA fees, and other costs can still change, but the loan’s base rate does not reset.

With an ARM, the early payment may be lower, but the future payment can rise if rates are higher when the adjustment period begins. That is the trade-off buyers need to understand before choosing this option.

For Tampa Bay buyers, the decision should not be based only on the starting rate. You also need to look at your timeline, your comfort with risk, your expected income, your savings, and whether you could still afford the home if the payment increased later.

Affordability is still a major challenge for many buyers. Between home prices, mortgage rates, property taxes, insurance, HOA fees, and closing costs, the monthly payment can feel tight even for buyers with solid income.

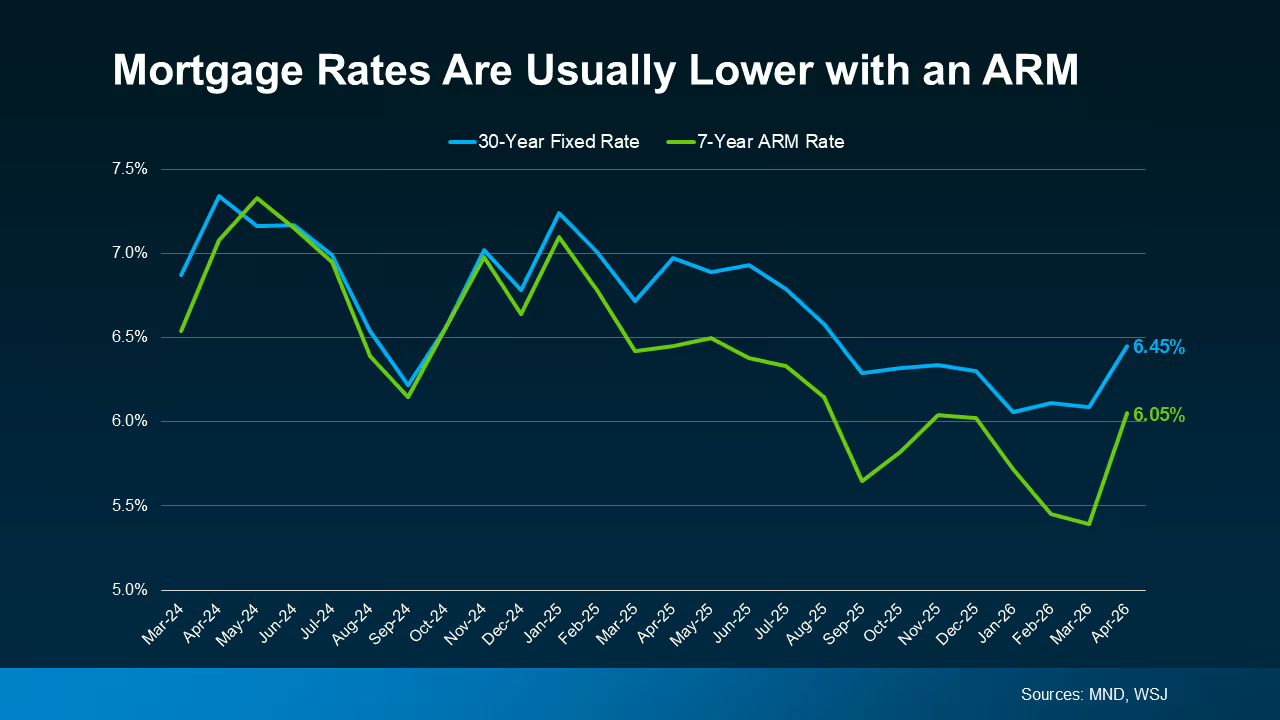

That is one reason adjustable-rate mortgages are getting more attention. In many cases, an ARM can offer a lower introductory rate than a 30-year fixed mortgage, which may reduce the initial monthly payment.

That lower starting payment can be appealing, especially for buyers trying to purchase in competitive areas of Hillsborough & Pinellas counties. A lower introductory rate may help some buyers qualify more comfortably or keep their monthly payment closer to their target range.

But the starting payment is only part of the story. The real question is whether the loan still makes sense when you look beyond the first few years.

When affordability gets harder, buyers often look for ways to reduce the monthly payment. Some choose a smaller home, a different location, a larger down payment, seller concessions, a temporary buydown, or a different loan type.

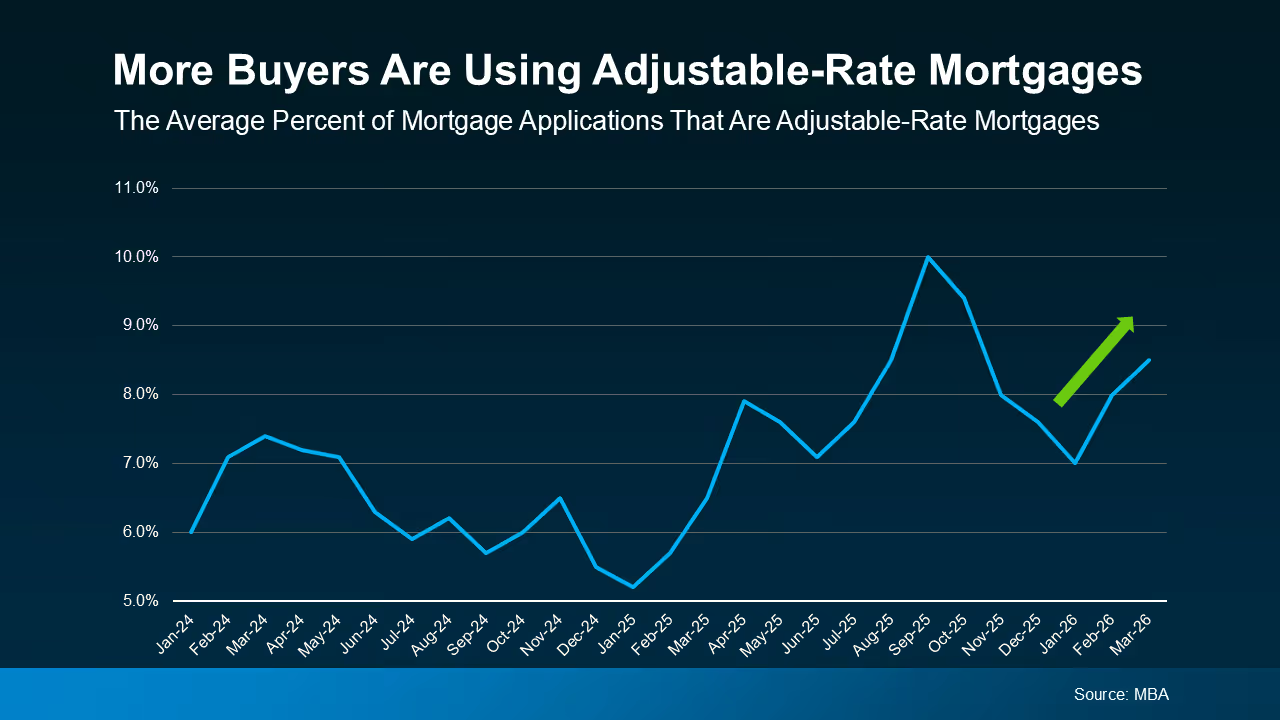

Others consider an adjustable-rate mortgage. The graph in the original article shows that the share of mortgage applications using ARMs has increased as buyers look for ways to manage affordability.

That does not mean ARMs are right for everyone. It simply means more buyers are weighing the short-term savings against the long-term uncertainty.

In areas like Tampa, St. Petersburg, Riverview, Brandon, Clearwater, Largo, Westchase, and FishHawk, the right financing strategy can depend heavily on the buyer’s plans. A buyer who expects to move in 5 years may view an ARM differently than a buyer who plans to stay in the home for 20 years.

The biggest risk with an ARM is that the payment can change after the fixed period ends. If market rates are higher at that time, the interest rate and monthly payment may increase.

Most ARMs have adjustment rules and rate caps. These caps can limit how much the rate can rise at the first adjustment, how much it can change during later adjustments, and how much it can increase over the full life of the loan. That protection matters, but it does not mean the payment cannot become uncomfortable.

Buyers should ask the lender to explain the index, margin, adjustment schedule, first adjustment cap, periodic cap, lifetime cap, and the highest possible payment. Those details are not just technical fine print. They determine how much risk you are taking on.

Before choosing an ARM, you should know the best-case, likely-case, and worst-case payment scenarios. If the highest possible payment would strain your budget, the lower starting rate may not be worth the risk.

An adjustable-rate mortgage may make sense for some buyers, especially if they have a clear plan. For example, a buyer who expects to sell before the first adjustment period may be less concerned about long-term rate changes.

It may also fit a buyer who expects income to rise, plans to pay the loan down aggressively, or has enough financial cushion to handle a higher payment later. In those situations, the lower introductory payment may provide useful flexibility.

But those plans need to be realistic. You should not choose an ARM only because you assume rates will fall or because you expect to refinance later. Refinancing depends on future rates, home value, credit, income, employment, and lending standards, none of which are guaranteed.

An ARM can be a tool, but it should not be a gamble. The loan should make sense even if the market does not move exactly the way you hope.

A fixed-rate mortgage may be a better fit if you want payment stability and plan to stay in the home long term. It can also be a better option if a future payment increase would create stress or make the home unaffordable.

Many buyers prefer knowing their principal & interest payment will remain steady. That predictability can make budgeting easier, especially for families balancing insurance, taxes, repairs, utilities, and everyday living costs.

A fixed-rate loan may not always offer the lowest starting payment, but it can provide more long-term certainty. For some buyers, that peace of mind is worth more than the initial savings from an ARM.

The right answer depends on your goals, not just the rate quote. A strong lender should be able to compare both options clearly so you can decide which one fits your budget & timeline.

Adjustable-rate mortgages are getting more attention because they can offer a lower starting payment at a time when affordability is still tight. For some buyers, that can make the difference between waiting and moving forward.

But ARMs are not automatically better, and they are not right for every buyer. The starting rate may be lower, but the future payment can change, and refinancing later is not guaranteed.

Before choosing an ARM, make sure you understand the adjustment schedule, rate caps, worst-case payment, and how long you realistically plan to keep the home. The best mortgage is not just the one with the lowest starting rate. It is the one that fits your finances, your risk tolerance, and your long-term plan.