Affordability is the relationship between home prices, mortgage rates, and income. In 2026, the biggest improvement is expected to come from more predictable mortgage rates and more homes for sale, not from a price crash.

In Tampa Bay, that matters because monthly payment is usually the deal breaker. Even small changes in rate, price, or seller concessions can move a payment enough to change what a buyer can qualify for.

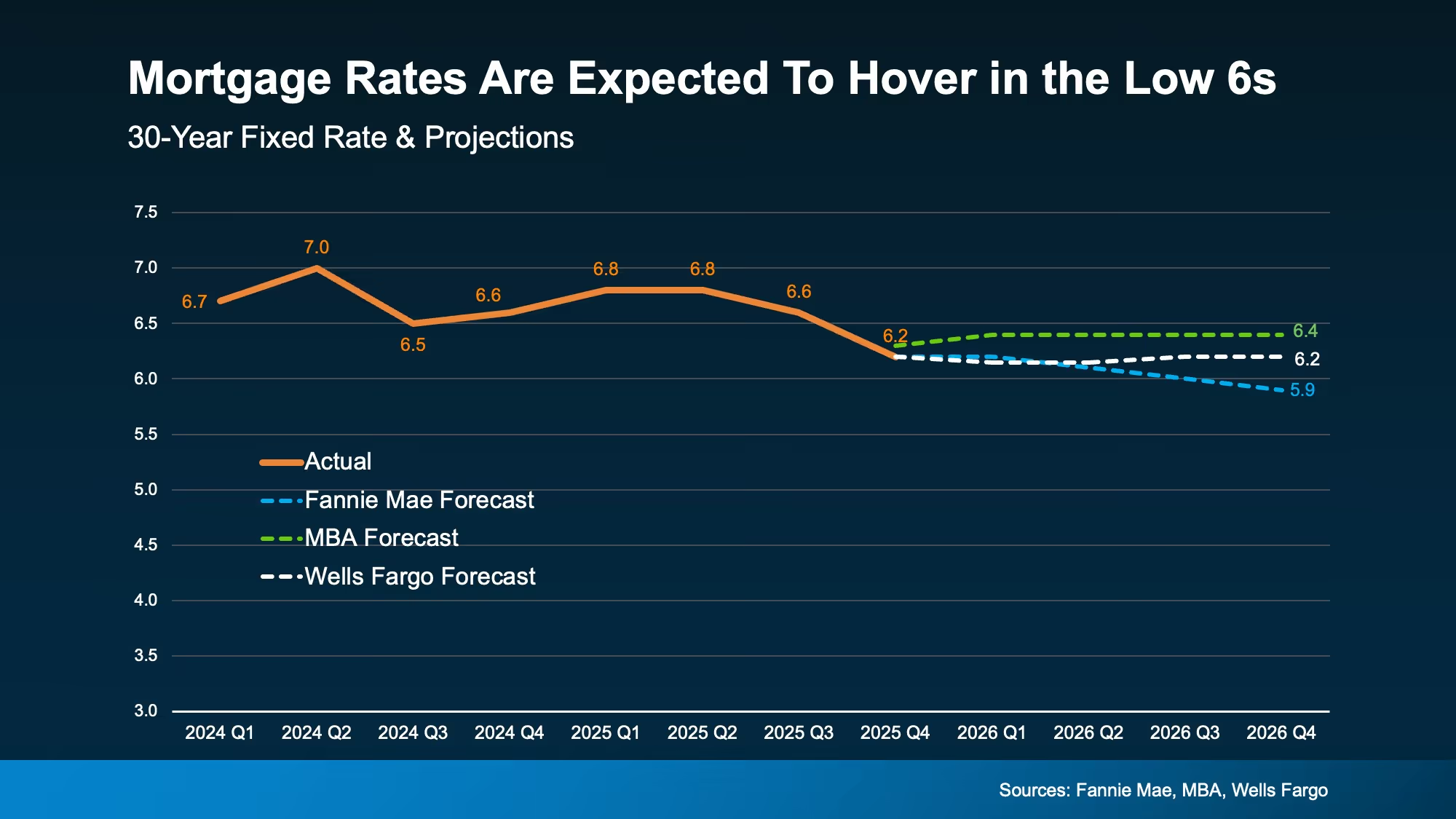

Most forecasts point to mortgage rates staying relatively stable, with many projections clustering in the low 6% range for much of 2026.

What this can mean locally:

Buyers get fewer sudden payment spikes while shopping.Sellers face fewer “rate shock” moments that freeze demand.

Practical move: if you are planning to buy in 2026, treat rate swings as a strategy, not a surprise. A lender can show payment scenarios at 5.75%, 6.25%, and 6.75% so you know your comfort zone before you negotiate.

When there are more options, buyers regain time and negotiating power. That can show up as:

Locally, inventory can vary sharply by price point and neighborhood. Some areas may feel balanced while others are still tight. The key is to track what is happening in the specific zip codes you are targeting, not just national headlines.

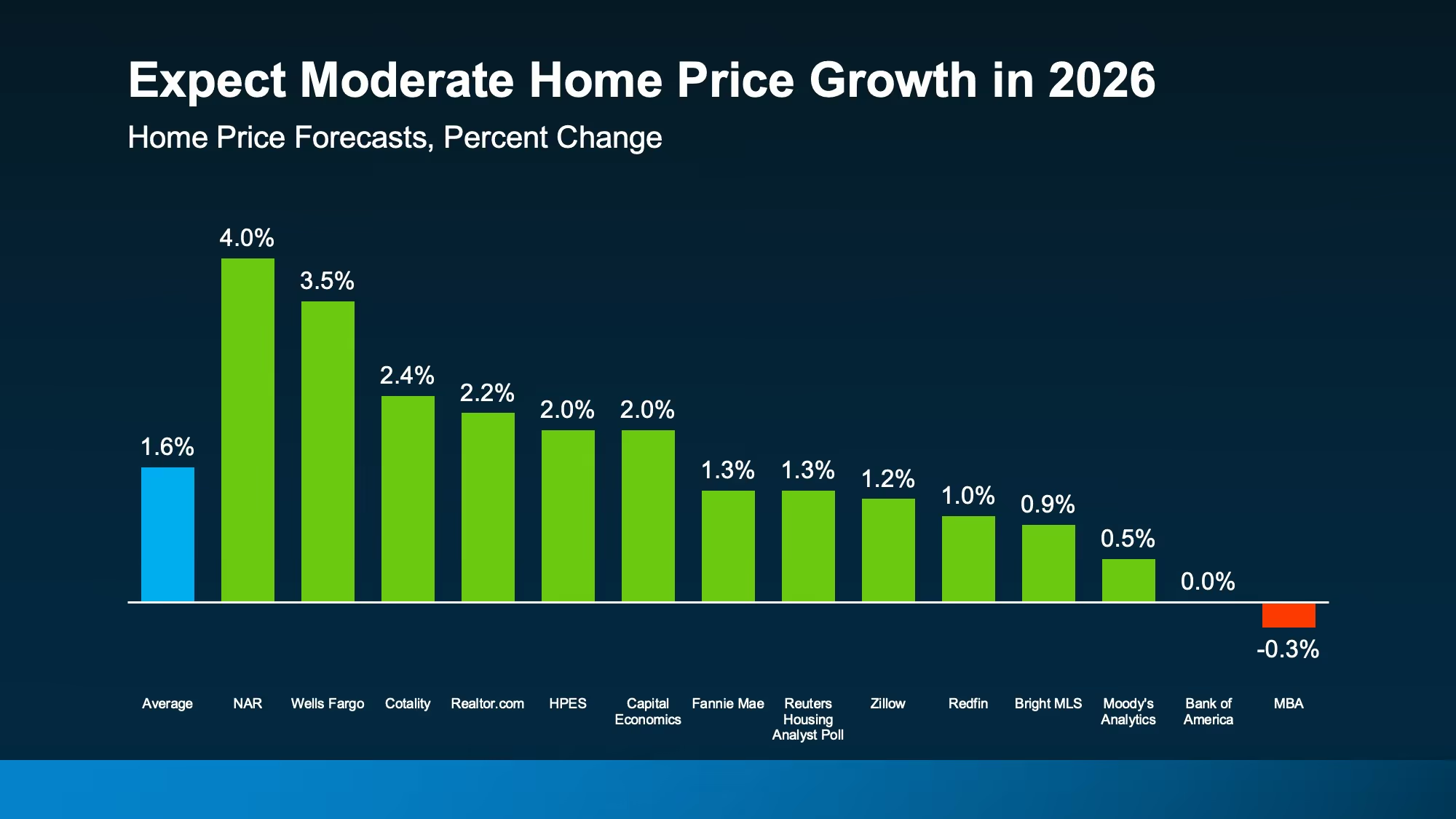

Many forecasts still call for prices to rise in 2026, but at a slower pace. A slower pace can be healthier because it reduces the pressure to overbid and helps buyers plan.

What this can mean in practice:

If you are seeing fear based content about prices “crashing,” compare it to what is actually happening in the neighborhood you care about, including active competition, price reductions, and days on market.

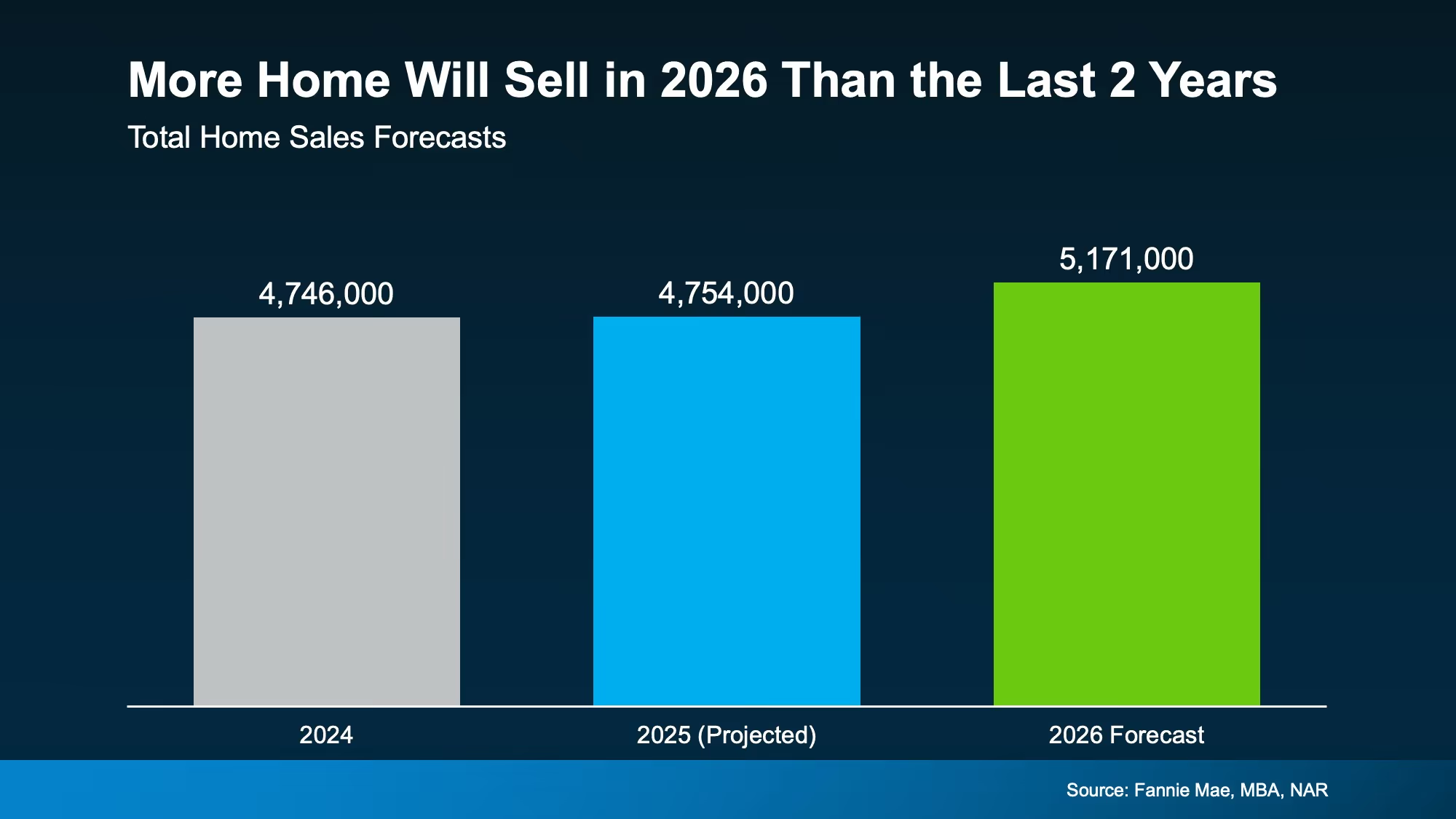

When affordability improves and inventory rises, more people can move. That typically increases transactions.

In Tampa Bay, more sales also means more comparable data for pricing and appraisals, which helps both sides make cleaner decisions.

Ask a lender for a payment breakdown that includes taxes, insurance, HOA, and estimated closing costs. In Florida, insurance and HOA can swing the payment more than people expect.

When inventory is higher, you can negotiate more effectively. Focus on the items that improve your long term cost, such as:

Buyers get fewer sudden payment spikes while shopping.Sellers face fewer “rate shock” moments that freeze demand.

Even in a more balanced market, the best homes still get attention. A clean preapproval and a clear plan help you win without overpaying.

The biggest mistake in a shifting market is pricing based on last year’s peak comps. Pricing should reflect current competition, current buyer expectations, and current days on market.

In a market with more options, condition matters more. Small improvements that reduce buyer objections can protect your net more than an aggressive list price.

A targeted concession can expand the buyer pool and reduce the chance of price cuts later. The best approach depends on your timeline and the competition in your neighborhood.